22 2 月

Bangladesh sits in a region where green, social, sustainability, and sustainability-linked instruments have steadily moved from niche pilots to mainstream funding channels. Globally, labelled sustainable debt has matured into a repeat-issuance market. Climate Bonds recorded USD 1.05 trillion of aligned GSS+ deals priced in 2024, marking a record year for aligned issuance. (https://www.climatebonds.net/data-insights/publications/global-state-market-2024)

Yet Bangladesh’s own thematic bond pipeline remains thin and episodic, even though the country has no shortage of investment needs that fit thematic use-of-proceeds labels—especially across infrastructure, inclusive development, and essential service delivery. A common assumption is that the gap is primarily about policy: taxonomy definitions, regulatory prioritization, or the absence of clear incentives. Those issues do matter. But in practice, Bangladesh’s pipeline often collapses earlier—at the point where an issuer must justify upfront credibility costs such as governance, frameworks, external review, and data systems before it has certainty of execution.

If Bangladesh wants thematic bonds to become a repeatable market category rather than a series of isolated headlines, it needs a bridge that reduces first-mover costs, standardizes execution, and turns learning-by-doing into a replicable playbook. The fastest way to build that bridge is a structured technical assistance and cost-sharing facility designed to produce multiple issuers per cycle.

The pipeline problem is not demand. It is pre-issuance friction.

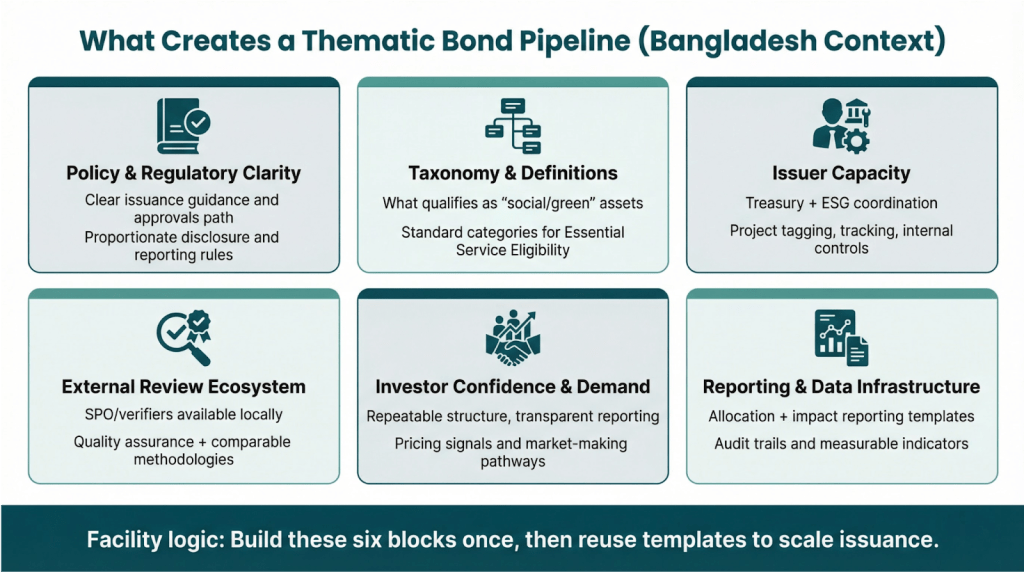

Thematic bonds are sometimes described as a label. For issuers, they function more like an operating capability—internal systems and controls that must be built before the market will trust the instrument and price it efficiently. Three structural gaps tend to reinforce each other in Bangladesh.

First is the capacity gap. Many institutions still lack in-house experience to design a thematic framework, align it with widely used principles, commission an external review, and then run allocation and impact reporting with discipline over time. Bangladesh’s policy direction on sustainable finance has strengthened over the past few years, including central bank-led sustainable finance policy frameworks referenced in international diagnostics of Bangladesh’s progress. (https://documents1.worldbank.org/curated/en/099651506132224594/pdf/IDU0d89fefd504c6f0460209dbe0dc187c4e6c5e.pdf)

Second is the information gap. Even motivated issuers often struggle to answer basic investor questions quickly. What is the eligible pool? How is eligibility determined? How will proceeds be tracked? Which KPIs will be reported, and with what data quality controls? Without a credible asset register and reporting plan, thematic bonds become harder to market—especially to institutions that must defend integrity to their own investment and risk committees.

Third is the cost gap, and it is often the decisive one. For first-time issuers, the biggest hurdle is spending money before the deal is real. Advisory work, legal structuring, framework drafting, external review such as an SPO, and the initial reporting architecture all come before execution. These are board-visible costs with uncertain payoff, so they get deprioritized.

Figure 1: Key pillars of thematic bond pipeline in the context of Bangladesh

The policy layer readers expect and why it is not the whole story

The title of this article naturally raises policy questions. Do regulations clearly define what qualifies? Is there a credible taxonomy? Do approval pathways support replication?

There are real enabling-environment considerations. Definitions and eligibility rules matter because ambiguity undermines investor confidence, particularly for mixed-use assets and blended portfolios. Bangladesh has already taken steps to formalize aspects of debt securities issuance and definitions around instruments such as green bonds, which helps create a base layer of shared language and disclosure expectations. (https://sec.gov.bd/slaws/Notification_01.06.2021.pdf)

Just as important is predictability. When approval timelines are uncertain, treasuries tend to deprioritize labelled issuance, especially if it is perceived as extra work. Credibility infrastructure also matters. That includes consistent expectations for external review and reporting, standardized templates, and clear accountability for how proceeds are tracked.

But policy development is rarely instantaneous, and it often advances through market feedback. That is why the most practical approach is not policy first then deals later, or deals first then policy later. It is co-evolution. An execution engine can produce real issuances and reporting cycles, while regulators learn what to standardize and where modest incentives have the highest payoff.

Why essential services are the ideal wedge to build a pipeline

If Bangladesh wants a thematic bond category that can repeat, the most pragmatic wedge is essential services sectors where financing expands access to foundational services households and communities rely on, and where outcomes can be defined, tracked, and reported in a credible way. This includes areas such as primary healthcare access, affordable housing, education-related financing, clean energy access, and climate-resilient municipal services. The goal is not to privilege one sector, but to focus on a category where the economics of aggregation, measurability, and governance make issuance more replicable.

Essential service investments often carry long payback periods and benefits that accrue over time. Yet much of Bangladesh’s financial intermediation remains anchored in shorter tenor liabilities, creating the classic asset–liability mismatch. Financing long-duration assets with short-duration funding elevates rollover risk and constrains scale especially where service delivery requires sustained maintenance, phased expansion, and predictable funding over multiple years.

Thematic bonds help reduce this friction by enabling longer, more stable tenors and by creating a disciplined mechanism to ring-fence proceeds, allocate them to a defined eligible portfolio, and report on both allocation and outcomes. Essential services are also naturally portfolio-able. Issuers can aggregate many eligible sub-loans or sub-projects under a unified framework, supporting diversification and clearer reporting. Once the first issuance establishes a credible template eligibility rules, governance, allocation tracking, and impact KPIs the marginal cost of future issuances falls. That is what pipeline economics looks like.

The fastest solution: a challenge-fund style TA and cost-sharing facility

A thematic bond pipeline is built through repetition. The practical question is how Bangladesh moves from scattered ambition to repeatable execution without requiring each institution to reinvent the issuance process. A facility model can do that by combining a transparent intake mechanism, disciplined cost-sharing, and embedded execution support—while keeping governance credible for both regulators and the market.

A clear host and governance model. The facility works best when run by an independent secretariat, for example a donor-backed platform housed within a neutral market institution or consortium, supported by a steering structure that includes key stakeholders. Regulators are most useful in an observer and advisory role helping align standards, documentation expectations, and approval-path predictability rather than selecting winners, which can create avoidable conflicts.

Call for proposals with explicit, bankable selection criteria. Cohorts should be selected against practical criteria. That includes an identifiable eligible asset pipeline for example an essential services portfolio (such as health access, affordable housing, education-related lending, clean energy access, or municipal resilience services) senior management commitment and internal governance, minimum data availability for tracking and reporting, a realistic issuance route and timeline, and willingness to co-finance costs and disclose progress. This turns the facility from a grant program into a pipeline engine.

Milestone-linked cost-sharing that is meaningful but capped. The facility should reimburse a defined share of eligible pre-issuance costs, often best framed as an indicative range such as 30 to 60 percent, with a per-issuer cap, and only when milestones are met. Milestones can include framework and governance approvals, eligible asset register validation, external review completed, proceeds tracking and reporting architecture established, and issuance documentation prepared. This reduces first-mover friction while preserving issuer ownership and avoiding subsidy dependence.

Embedded TA that delivers execution, not workshops. Technical assistance should be structured as end-to-end delivery support. This includes translating the issuance objective into a credible framework, setting up internal committees and controls, coordinating external reviewers and arrangers, and institutionalizing allocation and impact reporting. To reduce repeat costs, the facility can maintain a pre-qualified panel of reviewers and advisors and provide standardized templates that issuers can adapt rather than build from scratch.

Acknowledging the market reality: execution needs investor and arranger coordination too. Issuance readiness is necessary, but not sufficient. The facility should also support the last mile of execution. That includes arranger coordination, investor materials, and early investor engagement, including potential anchor participation where appropriate. This is often the difference between a ready framework and an executed deal.

Safeguards so the facility stays credible. Disbursements should remain strictly milestone-based, with stop rules if an issuer stalls and consequences for misrepresentation, such as disqualification from future cohorts and, where appropriate, clawback provisions. These safeguards protect integrity and reassure both donors and the market that the facility is building real capacity—not sponsoring labels.

Policy accelerators that work because they are modest

A facility becomes far more powerful when paired with targeted policy accelerators that reduce friction without distorting the market.

International precedents show that small incentives can unlock private issuance at scale by directly addressing early-stage costs. Singapore’s Sustainable Bond Grant Scheme is designed to support eligible expenses including external review and reporting-related work. (https://www.mas.gov.sg/schemes-and-initiatives/sustainable-bond-grant-scheme) Hong Kong’s Green and Sustainable Finance Grant Scheme, launched in 2021 and later extended through 2027, similarly subsidizes eligible issuance and external review expenses to deepen market activity. (https://www.fstb.gov.hk/fsb/en/business/funding_schemes/green-and-sustainable-finance-grant-scheme.html)

Bangladesh can adopt the underlying design logic rather than copy-pasting details. That includes clearer templates for reporting, predictable processing pathways for labelled instruments that meet defined criteria, and rationalization of frictions that disproportionately hurt first-time issuers. The aim is not to subsidize the bond market indefinitely. It is to buy down the learning curve so replication becomes commercially rational.

Post-LDC graduation: why the financing transition is not abstract

Bangladesh is scheduled to graduate from Least Developed Country status on 24 November 2026. (https://www.un.org/ldcportal/content/bangladesh-graduation-status) While the exact financing implications vary by instrument and partner, the transition is widely understood to make concessionality and preferences harder to access and to raise the importance of durable domestic financing channels—especially for long-horizon sectors like infrastructure and essential services. (https://cpd.org.bd/bangladeshs-decision-on-ldc-graduation-deferral-needs-careful-assessment/)

In that environment, domestic capital markets are no longer a technical ambition. They become a financing necessity. Thematic bonds, done with credible governance and reporting, are one of the clearer ways to connect domestic pools of capital to long-duration development needs, while creating a structure that DFIs and impact investors can more easily participate in.

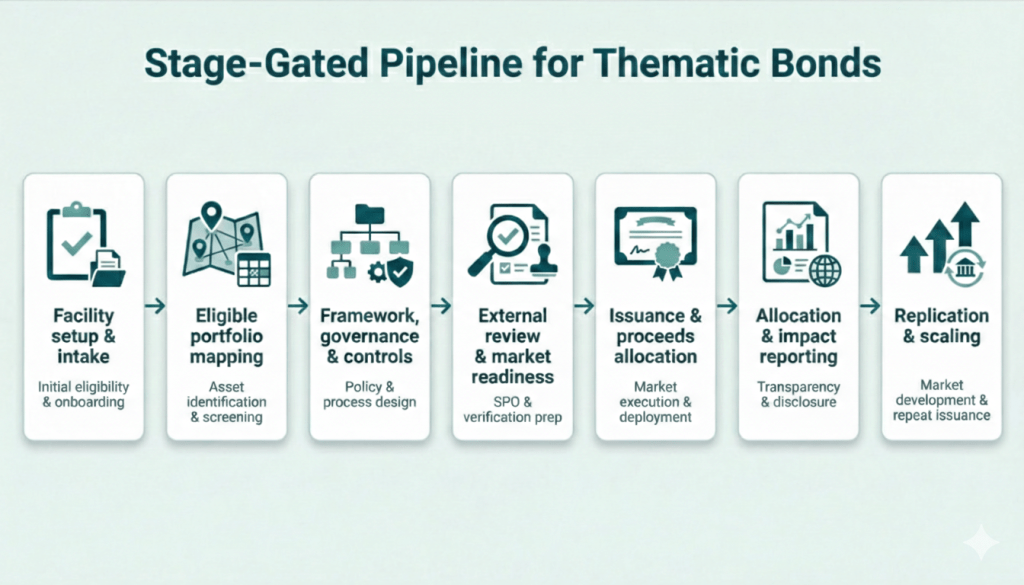

What a stage-based pipeline build looks like in practice

Pipeline building should be judged by outputs, not by calendar time. A practical facility therefore works best as a stage-gated process, where each issuer (and each cohort) progresses only when a defined set of deliverables is met. This keeps the approach realistic across institutions with different starting capacities, approval cycles, and market windows.

Stage 1: Facility setup and market intake

The facility establishes governance, eligibility standards, a pre-qualified panel of external reviewers and advisors, and a transparent call-for-proposals process. Issuers are screened for core readiness signals: senior management sponsorship, an identifiable eligible portfolio aligned to essential services, and basic data availability to support tracking and reporting.

Stage 2: Portfolio identification and eligibility architecture

Selected issuers translate ambition into a concrete eligible asset pipeline. This stage produces the building blocks investors care about early: eligibility rules, exclusions, portfolio mapping, and an auditable asset register that can be maintained over time. It also aligns internal roles so credit, treasury, sustainability teams, and internal audit understand how the portfolio will be governed.

Stage 3: Framework, governance, and controls

The issuer develops a credible thematic bond framework, including governance arrangements (committees, approvals, conflict management), proceeds management procedures, and the monitoring plan for allocation and impact reporting. This stage is where “label” becomes “operating capability”: the internal control environment is designed so it can withstand scrutiny, not only for issuance day but for the reporting cycle that follows.

Stage 4: External review and market readiness

The framework is subjected to an external review (for example an SPO or equivalent), while the issuer prepares execution documentation and investor materials. The facility’s role is to reduce friction—standardize templates, coordinate reviewers and arrangers, and ensure disclosure quality—so issuers do not reinvent every component.

Stage 5: Issuance execution and proceeds allocation

The bond is executed through the agreed route, and proceeds are allocated to the eligible portfolio through the tracking mechanism established earlier. This stage tests whether the portfolio design is operationally usable: can the issuer allocate smoothly, document decisions, and maintain traceability?

Stage 6: Allocation and impact reporting cycle

Reporting becomes the proving ground. Allocation reporting validates integrity; impact reporting demonstrates outcomes and strengthens investor confidence. This stage also generates the market learning regulators and stakeholders need to refine templates, harmonize expectations, and reduce ambiguity for the next cohort.

Stage 7: Replication and scaling

The facility’s ultimate output is not one issuance but a reusable issuance template that lowers marginal cost over time. Stage-gated learnings are consolidated into standardized tools—eligibility checklists, reporting templates, reviewer panels, and governance playbooks—so subsequent issuers can move faster with fewer bespoke costs.

Bangladesh does not need perfect market conditions before it can build a thematic bond pipeline. It needs a repeatable system that converts first-time friction into second-time efficiency—using real transactions and real reporting cycles to institutionalize credibility. A structured TA and cost-sharing facility, anchored in an essential services focus, offers a realistic path from isolated issuance to a durable market category.

References

- Climate Bonds Initiative. Global State of the Market 2024. https://www.climatebonds.net/data-insights/publications/global-state-market-2024

- UN LDC Portal. Bangladesh graduation status. https://www.un.org/ldcportal/content/bangladesh-graduation-status

- Monetary Authority of Singapore. Sustainable Bond Grant Scheme. https://www.mas.gov.sg/schemes-and-initiatives/sustainable-bond-grant-scheme

- Financial Services and the Treasury Bureau, Hong Kong. Green and Sustainable Finance Grant Scheme. https://www.fstb.gov.hk/fsb/en/business/funding_schemes/green-and-sustainable-finance-grant-scheme.html

- World Bank. Bangladesh country progress report referencing Bangladesh Bank sustainable finance policy elements. https://documents1.worldbank.org/curated/en/099651506132224594/pdf/IDU0d89fefd504c6f0460209dbe0dc187c4e6c5e.pdf

- Bangladesh Securities and Exchange Commission. Notification on debt securities rules including green bond definition and requirements. https://sec.gov.bd/slaws/Notification_01.06.2021.pdf

- Centre for Policy Dialogue. Note on Bangladesh LDC graduation transition considerations. https://cpd.org.bd/bangladeshs-decision-on-ldc-graduation-deferral-needs-careful-assessment/