18 Mar

Bangladesh stands at a critical juncture in its energy trajectory. Over the past decade, the nation has transitioned from relying almost entirely on domestic natural gas — which once fueled over 70% of its primary energy consumption — to becoming structurally dependent on imported Liquefied Natural Gas (LNG). This transformation, initially conceived as a temporary bridge to sustain rapid industrialization and economic growth, has evolved into a permanent fixture of the national energy architecture.

This first article in the series traces the origin of that dependency: the declining domestic reserves that made LNG imports inevitable, the pragmatic pivot from grand land-based terminal ambitions to Floating Storage and Regasification Units (FSRUs), the painful lessons of the COVID-19 price windfall and the Russia-Ukraine shock, and the scramble for long-term supply contracts that followed. It ends with Bangladesh entering 2026 seemingly better-positioned — only to be blindsided by the closure of the Strait of Hormuz.

“What began as a pragmatic response to declining domestic gas reserves has evolved into a structural dependency that threatens the nation’s economic sovereignty, fiscal stability, and energy security.”

The central argument of this series is that Bangladesh’s LNG dependency is no longer a stopgap — it is structural — and that a decade of policy choices prioritizing short-term expediency over long-term resilience has created a crisis that is not merely cyclical but existential for the country’s economic sovereignty.

The Prelude: Declining Domestic Reserves

For much of its post-independence history, Bangladesh was fortunate to possess substantial domestic natural gas reserves. Concentrated primarily in the northeastern Sylhet and Chattogram divisions, these reserves powered the nation’s economic transformation — supplying feedstock for fertilizer production, fueling the textile and ready-made garment (RMG) industries, and generating the bulk of the country’s electricity. At its peak, domestic gas met nearly all of the nation’s energy needs, providing a significant competitive advantage for Bangladeshi industries in global markets.

By the early 2010s, however, the signs of depletion were unmistakable. Production from major fields such as Bibiyana, Titas, and Habiganj had either plateaued or begun to decline. New discoveries were failing to keep pace with extraction rates. The country’s proven reserves, estimated at approximately 11.9 trillion cubic feet (Tcf) by Petrobangla, were being consumed at a rate that suggested exhaustion within two decades. Meanwhile, demand was surging, driven by population growth, urbanization, and the government’s ambitious GDP and industrialization targets.

It was against this backdrop that the concept of LNG imports first entered the national energy discourse. The Power System Master Plan (PSMP) 2010, and more significantly its 2013 update, formally acknowledged that domestic gas production alone could not sustain the country’s energy needs. The plan identified LNG imports as a necessary supplement to bridge the growing deficit. This was a watershed moment — the first official recognition that the era of self-sufficiency in natural gas was ending.

The Land-Based Terminal Dream: Matarbari and the Road Not Taken

The initial vision for LNG importation centred on large-scale, land-based regasification terminals. The government identified Matarbari Island in Cox’s Bazar district as the primary site. A land-based terminal offered compelling advantages: higher throughput capacity, greater operational longevity (30–40 years versus 15–20 for FSRUs), lower long-term operating costs, and more efficient integration with onshore pipeline networks.

The proposed Matarbari LNG Terminal was envisioned with an initial capacity of 7.5 MTPA, expandable to 15 MTPA. The Japan International Cooperation Agency (JICA) was involved in early planning, and Tokyo Gas was later awarded a feasibility study contract in 2021 to assess technical and commercial viability.

However, formidable obstacles stood in the way. The estimated capital cost of $3–5 billion was daunting for a country with limited fiscal headroom. Land acquisition in the densely populated coastal region proved politically and logistically complex. Environmental impact assessments raised concerns about the ecological sensitivity of the area. Most critically, the construction timeline — estimated at 5–7 years from final investment decision to first gas — was incompatible with the urgency of the energy deficit. Bangladesh needed gas immediately, not in the mid-2020s.

The Matarbari land-based terminal remains, as of 2026, in the planning and feasibility stage. It has not reached a final investment decision, and the recent geopolitical disruptions have cast further uncertainty over its future. The project stands as a symbol of the enduring tension between long-term strategic planning and the short-term imperatives that have repeatedly shaped Bangladesh’s energy decisions.

The Pivot to FSRUs: Speed Over Scale (2014–2017)

Faced with the impracticality of waiting for a land-based terminal, the government made a pragmatic decision to pursue Floating Storage and Regasification Units (FSRUs) as the primary import mechanism. FSRUs — essentially converted LNG carriers equipped with onboard regasification facilities — could be deployed in a fraction of the time required for onshore construction, moored at offshore or nearshore locations, and connected to the existing gas pipeline network via subsea pipelines.

The pivotal agreement came in June 2014, when Petrobangla signed a 15-year charter agreement with US-based Excelerate Energy for the provision of an FSRU at Moheshkhali Island. The FSRU, named Excellence, had a storage capacity of 138,000 cubic metres and a regasification capacity of 500 MMcfd (approximately 3.75 MTPA). A second FSRU project was awarded to Summit Group, a major Bangladeshi conglomerate, in partnership with Excelerate Energy, under a separate 15-year charter signed in August 2017.

Simultaneously, the government secured its foundational LNG supply contract. In September 2017, Petrobangla signed a 15-year Sales and Purchase Agreement (SPA) with RasGas — a Qatari joint venture between Qatar Petroleum and ExxonMobil, later absorbed into QatarEnergy — for the supply of 2.5 MTPA of LNG. This contract, priced on a slope linked to Brent crude oil, would provide the anchor volume for the new import infrastructure.

First Gas and Early Operations (2018–2019)

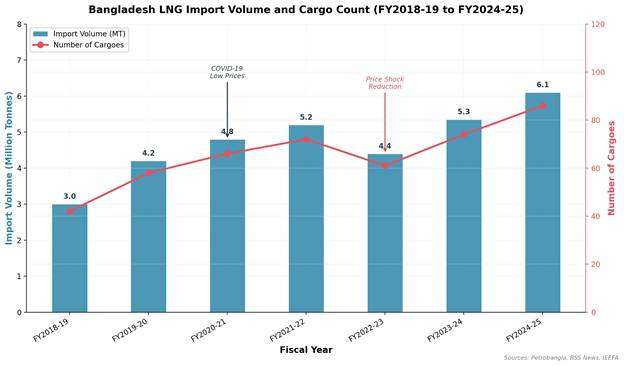

In August 2018, the Excelerate FSRU was commissioned and Bangladesh received its first commercial LNG cargo — a milestone celebrated as the beginning of a new era of gas supply diversification. In its first partial fiscal year (FY2018-19), Bangladesh imported approximately 3.0 million tonnes of LNG, primarily under the Qatari long-term contract.

In April 2019, the Summit FSRU commenced operations at a separate berth near Moheshkhali, bringing the total regasification capacity to approximately 1,000 MMcfd or 7.5 MTPA. With two FSRUs operational, Bangladesh had the infrastructure to import significant volumes of LNG. However, this period also saw the first signs of procurement challenges: negotiations with AOT Energy (a Swiss-based trading firm) for a medium-term supply contract were initiated but ultimately fell through; a similar arrangement with Trafigura was also abandoned — early indicators of the difficulties Bangladesh would face in securing competitive terms.

Figure 1: Bangladesh’s LNG import volumes and cargo counts from FY2018-19 to FY2024-25, showing the steady upward trajectory despite the FY2022-23 dip caused by the global price crisis.

The COVID-19 Paradox and the Russia-Ukraine Shock (2020–2022)

The period from 2020 to 2022 encapsulated the extreme volatility that characterises global LNG markets and the particular vulnerability of price-sensitive importers like Bangladesh.

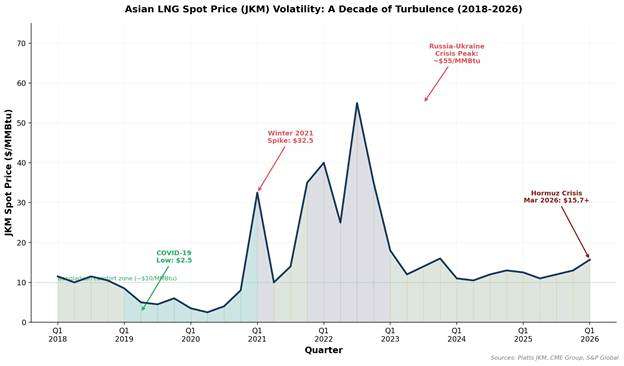

The onset of the COVID-19 pandemic in early 2020 caused a dramatic collapse in global energy demand. Asian LNG spot prices — measured by the Japan/Korea Marker (JKM) — plummeted to historic lows, falling below $2.50/MMBtu in mid-2020. For Bangladesh, this was a rare opportunity: spot market purchases were significantly cheaper than the cost of its long-term Qatari contract. The government increased spot purchases accordingly, and the experience reinforced a perception among some policymakers that the spot market could be a cost-effective procurement channel.

This perception was catastrophically overturned in the following two years. The global economic recovery from COVID-19, combined with supply chain disruptions, drove LNG prices sharply higher in late 2021. The JKM spiked to $32.50/MMBtu during the winter of 2021-22. Then, in February 2022, Russia’s invasion of Ukraine triggered the most severe energy crisis in decades. European nations, scrambling to replace Russian pipeline gas, entered the global LNG market as aggressive buyers, competing directly with Asian importers for available cargoes. JKM prices soared to unprecedented levels, peaking near $85/MMBtu in August 2022.

For Bangladesh, the consequences were devastating. At these price levels, spot market LNG was simply unaffordable. The government was forced to cancel or defer spot cargo purchases, leading to severe gas shortages, rolling blackouts affecting millions of households, and significant production losses in the RMG sector. In FY2022-23, total LNG imports fell by over 15% compared to the previous year — not because demand had decreased, but because the country could not afford to buy at prevailing market prices. According to analysis by Ember Energy, Bangladesh’s spot market LNG purchases were projected to cost approximately $11 billion between 2022 and 2024.

Figure 2: The extreme volatility of Asian LNG spot prices (JKM) from 2018 to 2026, highlighting the COVID-19 low, the Russia-Ukraine crisis peak, and the March 2026 Hormuz-related surge.

“The crisis laid bare the fundamental flaw in Bangladesh’s procurement strategy: an over-reliance on the spot market without adequate long-term contract coverage or strategic reserves to buffer against price shocks.”

The Scramble for Long-Term Contracts (2023)

The trauma of the 2022 price crisis catalysed a strategic recalibration. Recognising the imperative of securing stable, predictable supply, Petrobangla embarked on an aggressive campaign to sign new long-term SPAs.

In June 2023, QatarEnergy and Petrobangla signed a second 15-year SPA for approximately 1.5–1.8 MTPA of LNG, with deliveries commencing in early 2026, linked to the massive North Field East (NFE) expansion project in Qatar. This contract was priced at a slope of 13.35% of Brent crude plus a constant of $0.30/MMBtu — at a Brent price of $80/barrel, translating to approximately $11/MMBtu.

In November 2023, Excelerate Energy and Petrobangla signed a separate 15-year LNG supply agreement for 0.85 MTPA in 2026 and 2027, increasing to 1 MTPA from 2028 through 2040. This deal was significant not only for the additional volume but because it represented a diversification of supply beyond Qatar, as Excelerate sources LNG from a global portfolio of suppliers. According to S&P Global Commodity Insights, these new contracts were expected to bring Bangladesh’s total contracted LNG volume to approximately 7.2 MTPA by 2027.

Table 1: Bangladesh’s Active Long-Term LNG Supply Contracts (as of Early 2026)

| Contract | Supplier | Volume (MTPA) | Duration | Start Year | Pricing Basis |

| SPA 1 (2017) | QatarEnergy (formerly RasGas) | 2.5 | 15 years | 2018 | Brent-linked slope |

| SPA 2 (2023) | QatarEnergy (NFE) | 1.5–1.8 | 15 years | 2026 | 13.35% Brent + $0.30 |

| SPA 3 (2023) | Excelerate Energy | 0.85–1.0 | 15 years | 2026 | Brent-linked slope |

| Total Contracted | ~4.85–5.3 |

Cancellations and Consolidation (2024–2025)

Despite progress in securing long-term supply, the period of 2024–2025 was marked by significant project cancellations that reshaped the infrastructure landscape.

In October 2024, the government cancelled the planned second FSRU project by Summit Group, which would have added a third FSRU with a capacity of 4.5 MTPA. The cancellation was attributed to concerns about the financial terms of the charter agreement, questions about the necessity of additional floating infrastructure given the slow progress at Matarbari, and broader economic pressures on the government’s fiscal position.

In September 2025, the Summit LNG supply contract was also cancelled by Petrobangla. This left a gap in the supply portfolio that would need to be filled through alternative arrangements — likely from the spot market, the very channel that had proven so costly in 2022.

Despite these cancellations, the sheer volume of LNG imports continued to climb, driven by the relentless decline in domestic production. In calendar year 2025, Bangladesh imported a record 109 cargoes of LNG, totalling between 7.16 and 7.41 million tonnes, at a cost of approximately $3.88 billion — a 19% increase in volume and a 28% increase in expenditure compared to 2024, when 86 cargoes costing $3.02 billion were imported.

The March 2026 Hormuz Crisis: A Perfect Storm

The situation reached a critical inflection point in early March 2026. The escalation of the US-Israeli military campaign against Iran led to Iran’s closure of the Strait of Hormuz — the narrow waterway through which approximately 20% of global LNG trade flows.

For Bangladesh, the impact was immediate and cascading. QatarEnergy invoked force majeure on its contractual obligations on March 2, as all shipments from Ras Laffan must transit the Strait. OQ Trading (Oman) followed on March 5, and Excelerate Energy on March 6. Bangladesh was suddenly thrust into the global spot market at a time of extreme scarcity and panic, with spot prices surging from $10.73/MMBtu in late February to $15.70/MMBtu within days, and continuing toward $24–28/MMBtu. Bangladesh ultimately secured emergency spot cargoes at $28.28/MMBtu — approximately 2.5 times the pre-crisis level.

The crisis exposed every structural weakness in Bangladesh’s energy architecture simultaneously: the over-concentration of supply from a single geographic region, the absence of strategic storage, the inadequacy of domestic production, and the lack of alternative energy sources capable of substituting for gas-fired power generation at scale. The question of how this vulnerability was allowed to develop so deeply — and what can be done about it — is the subject of Part 2 of this series.

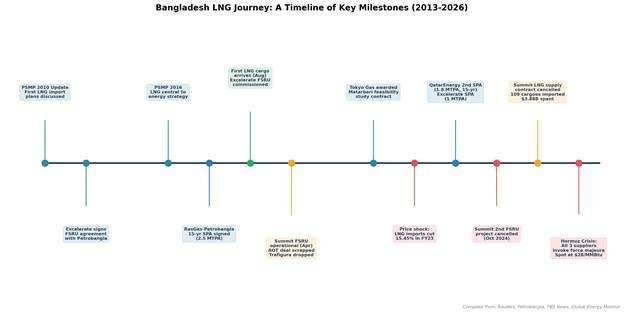

Figure 3: Key milestones in Bangladesh’s LNG journey from 2013 to 2026.

Table 2: Key Milestones in Bangladesh’s LNG Journey

| Year | Key Milestone |

| 2010–13 | PSMP formally acknowledges LNG imports as necessary to bridge domestic gas shortfall |

| 2014 | Petrobangla signs 15-year FSRU charter with Excelerate Energy at Moheshkhali Island |

| 2017 | Summit Group FSRU deal signed; 15-year SPA with RasGas/QatarEnergy for 2.5 MTPA |

| Aug 2018 | First LNG cargo received; Excelerate FSRU commissioned at Moheshkhali |

| Apr 2019 | Summit LNG FSRU begins operations; combined regasification capacity reaches 7.5 MTPA |

| 2020 | COVID-19 drives JKM to <$2.50/MMBtu; Bangladesh increases spot purchases |

| Aug 2022 | JKM peaks at ~$85/MMBtu (Russia-Ukraine crisis); Bangladesh forced to cancel spot cargoes |

| Jun 2023 | Second QatarEnergy SPA signed: 1.5–1.8 MTPA, 15-year, at 13.35% Brent slope |

| Nov 2023 | Excelerate Energy SPA signed: 0.85–1.0 MTPA, 15-year |

| Oct 2024 | Summit second FSRU project cancelled by government |

| Sep 2025 | Summit LNG supply contract cancelled by Petrobangla |

| Mar 1, 2026 | Iran closes Strait of Hormuz; QatarEnergy, OQ Trading, Excelerate invoke force majeure |

Coming Up in Part 2

Part 2 of this series — “The Anatomy of Vulnerability” — examines the structural problems that Bangladesh’s LNG journey has created. It will cover the accelerating decline of domestic gas production, the procurement dilemma between long-term contracts and the spot market trap, the extreme geographic concentration of supply from Qatar and the Middle East, the mechanics of the Hormuz chokepoint crisis, and the full financial picture — including the $18 billion cumulative import bill, the subsidy spiral, and the growing foreign exchange drain.