22 Feb

Labelled sustainable bonds have moved from the margins into the mainstream of global capital markets, and the scale is now large enough that investors treat them as a normal part of fixed-income allocation decisions rather than a niche product. Annual labelled sustainable bond issuance in 2024 reached USD 1.1 trillion, according to the World Bank’s market update. (The World Bank Docs) Another major market review similarly notes that global GSSS issuance topped USD 1 trillion in 2024, while also highlighting that the asset class’s share of total fixed income can move with broader market cycles. (IFC)

That “mainstreaming” is exactly why the market has also become more demanding. In 2025, green bond issuance and overall labelled issuance saw sharp slowdowns in some quarters, with market commentary pointing to a mix of regulatory uncertainty and shifting political signals that made some issuers hesitate. (Reuters) When appetite becomes more selective, the due diligence lens tightens. Investors start asking for fewer slogans and more proof.

Bangladesh is now navigating this same credibility test at an earlier stage of market development. The regulatory base is gradually strengthening, including the BSEC Debt Securities Rules (2021) that explicitly recognize issuance provisions for instruments such as green and blue bonds, and related regulatory processes around consent fees and approvals. (BSEC) Bangladesh Bank has also issued a dedicated Policy on Green Bond Financing for Banks and Financial Institutions, setting expectations on tenor, compliance, and process flow for banks and FIs engaging in green bond financing. (SBFN Data Portal)

In that context, landmark transactions matter beyond their size. BRAC Bank’s board approval for a Tk 1,000 crore social subordinated bond was an early public signal that a domestic thematic bond market could be executed. (The Daily Star) When the bank later secured approval from both BSEC and Bangladesh Bank, described publicly as Bangladesh’s first social bond, it effectively raised the bar for what “credible” needs to look like in practice. (The Daily Star)

This is the core point of the article. Investors do not buy the theme first. They buy the machine behind the theme. A thematic bond becomes investor-verifiable only when the promise can be checked through eligibility logic, governance, tracking, and reporting that hold up under scrutiny. The label may open the door, but the control system is what keeps it open.

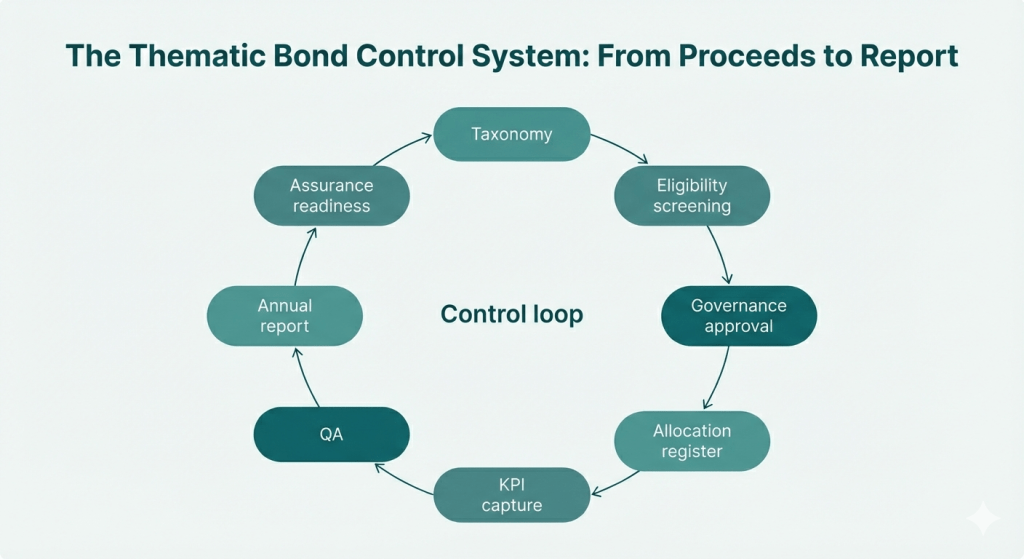

FIGURE 1: The Thematic Bond Control System, From Proceeds to Report

The credibility gap: why first-time issuers often stumble

Most thematic frameworks read well on paper. The failures are usually operational. Eligibility gets interpreted differently across branches. Documentation expectations are unclear, so evidence becomes inconsistent. Allocation tracking is treated like a narrative section rather than a ledger discipline. Reporting becomes a one-off project instead of an institutional cycle.

This is why investor-verifiable design is not mainly about writing better narratives. It is about engineering an operating system that turns intention into repeatability. Market standards reinforce this logic. The ICMA principles, widely used as a reference point across markets, emphasize four core components that must be demonstrable in practice: use of proceeds, evaluation and selection, management of proceeds, and reporting. (icmagroup.org)

1) Start with a taxonomy that can be executed, not admired

The first engineering decision is to define a taxonomy that can be applied at scale, not just explained in a framework. The “eligible category” language needs to translate into consistent screening decisions across teams and time.

An executable taxonomy tends to have three qualities.

It is specific enough to prevent drift. A category like “essential services” can expand into almost anything unless inclusion and exclusion rules are clear.

It is built around evidence, not opinion. The taxonomy should state what documents prove eligibility and what minimum data fields must be captured at origination so a third party can trace the decision later.

It is designed backwards from reporting reality. If the issuer promises KPIs it cannot measure without building an entirely new data pipeline, the reporting section becomes a future liability rather than a commitment.

2) Build governance that makes decisions consistent and reviewable

Investors quickly test whether governance is real by asking simple questions. Who decides what is eligible? On what basis? With what documentation? What happens when interpretations differ?

A credible governance model does not need to be bureaucratic. It needs to be disciplined. In practice that usually means a clear workflow from proposal to validation to approval, a documented rationale trail explaining why an asset is included, and escalation rules for edge cases. The investor-relevant signal is not the number of committees. It is whether decisions are reproducible and reviewable.

3) Treat management of proceeds as a ledger discipline

This is the backbone of verifiability. Investors want confidence that proceeds are allocated to eligible assets and that the issuer can prove it.

A practical instrument for that proof is an allocation register, which links proceeds to eligible loans or projects and captures dates, categories, allocated amounts, and any rules on refinancing versus new financing. This is not only a reporting tool. It is the control layer that makes reporting possible. The World Bank’s guidance on proceeds management and reporting captures the same practical direction: investors value transparency around allocation, and issuers benefit when the process is structured, traceable, and auditable. (The World Bank Docs)

If the register is strong, allocation reporting becomes routine extraction. If it is weak, everything downstream becomes reconstruction. Reconstruction is where credibility usually leaks out.

| Common failure mode | What it looks like in practice | Control(s) that prevent it |

| Vague eligibility criteria | Teams propose borderline assets; confusion over what “counts” | Eligibility inclusion/exclusion checklist + documented decision rules |

| Inconsistent interpretation across teams | Similar assets approved in one unit but rejected in another | Standard guidance note + training + QA sampling of decisions |

| Weak ring-fencing of proceeds | Proceeds mingle with general treasury; hard to prove “use of proceeds” | Allocation register + monthly reconciliation (proceeds vs allocations) |

| Misallocation / eligibility drift over time | Asset becomes ineligible later but stays “allocated” | Post-allocation monitoring + periodic re-eligibility checks |

| KPI inflation or “impact over-claiming” | Big numbers reported without traceable basis | KPI definitions + evidence rules + calculation templates + plausibility checks |

| Data gaps / missing borrower data | KPIs cannot be calculated; inconsistent datasets | Minimum data fields required at origination + data validation rules |

| Double counting (across products/projects) | Same loan counted twice in allocation or impact | Unique ID rules + de-duplication checks + register controls |

| Reporting delays / missed deadlines | Annual report slips; approvals not ready | Reporting calendar with owners + milestones + sign-offs |

| Governance gaps / unclear approvals | Decisions made informally; hard to show accountability | Governance approval workflow (committee/approver matrix) |

| Weak audit / assurance readiness | External reviewer can’t trace claims end-to-end | Assurance-ready document pack + traceability mapping |

TABLE 1: “Common Failure Modes vs Controls That Prevent Them

4) Make reporting repeatable: build a KPI library with definitions and evidence rules

Investors increasingly treat labelled instruments as standard fixed-income holdings, which means reporting is expected to be consistent and auditable, not expansive.

The most practical approach is to create a KPI library that acts as a single source of truth. It defines what the indicator means, what is counted, what is excluded, where the data comes from, how often it is collected, and what evidence supports it. This prevents a common failure where KPIs “shift” each year based on convenience rather than comparability.

For many first-time issuers, the reporting breakthrough comes from choosing a small number of indicators and running them with integrity. Stable definitions and transparent limitations matter more than ambitious but fragile measurement.

5) Design for assurance readiness from day one

Even when formal external assurance is not immediate, the market expectation is moving toward more verification and higher-quality disclosure. The ICMA guidance encourages transparency and recommends external review and post-issuance verification practices that strengthen market confidence over time. (icmagroup.org)

Assurance readiness can be built through a few straightforward disciplines. Eligibility decisions are documented in standard formats. Allocations reconcile to financial records. KPI calculations trace back to source data. A basic QA routine exists, using sampling, exception logs, and periodic reviews. When those elements are embedded early, annual reporting becomes an institutional cycle. When they are not, annual reporting becomes a scramble.

A short vignette: when a WASH carve-out becomes credible

WASH is often cited as a high-impact “essential services” theme. In practice, it becomes investable only when it is operationalized.

In one thematic bond preparation effort, a WASH carve-out could not rely on broad sector labels. It required ring-fenced eligibility logic describing what counts as WASH lending and what does not, plus a documentation pack that frontline teams could apply consistently. It also required a KPI set that could be reported annually without building a parallel bureaucracy. The credibility gain did not come from adding WASH to a framework. It came from making WASH eligibility auditable and WASH outcomes reportable.

That is the pattern. Thematic carve-outs fail less because they lack relevance and more because they are not engineered.

The minimum viable credibility stack

A first-time issuer does not need perfection. It needs a system that is clear, testable, and repeatable.

- Executable taxonomy with inclusion and exclusion rules, plus evidence requirements

- Governance workflow with defined roles, sign-offs, and escalation

- Allocation register enabling ring-fencing and reconciliation discipline

- KPI library defining indicators, sources, and collection frequency

- QA routine using sampling, exception logs, and periodic reviews

- Reporting calendar with owners, deadlines, and approvals

- Assurance readiness built through traceability and documentation

The larger lesson is simple. Thematic bonds are not only funding instruments. They are governance commitments. In an early-stage market, the issuers that build investor-verifiable systems are the ones most likely to turn a first transaction into a repeatable category.

References

- World Bank Treasury, Labeled Bond Quarterly Newsletter (Issue No. 10) (includes 2024 annual labelled sustainable bond issuance figure). (The World Bank Docs)

- IFC, Emerging Market Green Bonds 2024 (market size context and issuance dynamics). (IFC)

- Reuters, Green bond issuance dives almost a third amid climate backtracking (2025 issuance slowdown and market uncertainty context). (Reuters)

- Reuters, Politics, not climate, to drive sustainable finance trends in 2025 (regulatory and political uncertainty shaping the market). (Reuters)

- Bangladesh Securities and Exchange Commission, Debt Securities Rules notification (with green/blue bond provisions). (BSEC)

- Bangladesh Bank, Policy on Green Bond Financing for Banks and FIs. (SBFN Data Portal)

- The Daily Star, BRAC Bank to issue Tk 1,000 crore bond (board approval announcement). (The Daily Star)

- The Daily Star, BRAC Bank gets approval for Bangladesh’s first Social Bond (regulatory approvals). (The Daily Star)

- ICMA, Green Bond Principles (June 2025 update) (core components and reporting expectations). (icmagroup.org)

- ICMA, Social Bond Principles (core components and external review expectations). (icmagroup.org)

- World Bank, Green Bond Proceeds Management and Reporting Guide (practical proceeds management and transparency guidance). (The World Bank Docs)