18 3 月

Bangladesh is among the world’s most exposed countries to the Hormuz crisis. The vulnerability took a decade to build.

When the Strait of Hormuz closed in early March 2026, the images that came out of Dhaka were not the kind anyone associates with one of Asia’s fastest-growing economies. Long queues of motorcycles coiling around petrol stations. University campuses shuttered by government order, their Eid holidays brought forward by weeks as an emergency power-conservation measure. Fuel rationing introduced within days. Al Jazeera ran footage of pumps running dry in districts outside the capital. The Bangladesh Petroleum Corporation set per-vehicle refuelling limits to prevent hoarding. A country of 170 million people was scrambling for fuel.

The international coverage was quick and, in its way, accurate. Al Jazeera named Bangladesh among the countries facing the gravest risks from the disruption, citing a Centre for Global Development analysis that weighed energy import dependence, foreign exchange reserves, and public debt levels. The Diplomat observed that Bangladesh, Pakistan and Sri Lanka had spent years signing long-term Gulf LNG contracts to reduce their exposure to spot-market volatility, and that the Iran war had torn those contracts apart. The World Economic Forum’s energy tracker listed the university closures as a headline consequence of the crisis. S&P Global and IEEFA both placed Bangladesh, Pakistan and India among the Asian importers sourcing the largest share of their LNG from Qatar and the UAE, making them disproportionately dependent on a corridor that had just been shut. By most measures, Bangladesh was among the worst positioned countries on earth for what had just happened.

What almost none of that coverage explained was why.

Bangladesh’s place on those lists was not an accident of geography, or bad luck, or the unforeseen consequence of a war nobody predicted. It was the result of specific decisions, made across a decade, that built a particular kind of vulnerability into the country’s energy architecture. The Hormuz closure did not create the crisis Bangladesh is now navigating. It revealed one that had been accumulating since the country’s domestic gas fields began to run dry in the early 2010s, and that was deepened by every choice made in response.

For years before the crisis, the complaint from factory floors across Dhaka and Chittagong was about gas pressure. Not the price: gas in Bangladesh was subsidised and cheap by regional standards. But the pressure would drop at peak hours, slowing machines, stalling production lines. Business associations wrote letters. Industry bodies lobbied ministers. The problem was treated, almost universally, as a distribution issue. A pipe issue. Something that coordination and better infrastructure could fix. What those meetings rarely confronted was what was happening below the surface: the fields were running dry, and the gas that had let a country of 170 million people industrialise cheaply was being replaced, cargo by cargo, with imported LNG bought in dollars on global markets.

The businessmen who complained about gas pressure were not wrong. They were just, in most cases, measuring the wrong thing. This article is about what they were not measuring, and how it became the most important number in the country’s economic life. It is the first in a series on Bangladesh’s LNG dependency: how it was constructed, what it has cost, and what the Hormuz closure in March 2026 made visible about the decisions taken along the way.

| KEY FINDINGS — PART 1 | |

| Structural shift | Bangladesh moved from near-total domestic gas self-sufficiency to importing over 7 MTPA of LNG in under a decade. The import dependency is now hardwired into power generation, fertiliser production, and the garment export sector. |

| Infrastructure lock-in | The 2014 decision to use FSRUs delivered speed but sacrificed long-term economics. A land-based terminal at Matarbari, which would have been cheaper per unit over a 30-40 year lifespan, remains unbuilt in 2026. |

| Procurement fragility | Overreliance on spot LNG, encouraged by the COVID-era price collapse, was catastrophically exposed when Russia invaded Ukraine in 2022 and the JKM reached $85 per MMBtu. Bangladesh cut imports by over 15% against rising demand. |

| Geographic concentration | Roughly 75% of Bangladesh’s contracted LNG volume, as of early 2026, originates in or must transit the Persian Gulf. The March 2026 Hormuz closure activated force majeure across all three active long-term contracts simultaneously. |

| Fiscal pressure | Bangladesh spent approximately $3.88 billion on LNG imports in 2025, a 28% increase in expenditure over 2024, against declining foreign exchange reserves and a growing subsidy burden. |

“What began as a pragmatic response to declining domestic gas reserves has evolved into a structural dependency that now touches the price of electricity, the cost of fertiliser, the health of Bangladesh’s foreign exchange reserves, and the viability of its largest export industry.”

A Decade of Decisions: How Bangladesh Arrived Here

For much of its post-independence history, Bangladesh was fortunate to have natural gas beneath its feet. The reserves in Sylhet and Chattogram, the great fields of the northeast, powered the country’s transformation. Gas fuelled the generators that kept factories running. It fed the fertiliser plants that kept agriculture productive. It gave Bangladeshi exporters a cost advantage that neighbours could not easily match.

By the early 2010s that advantage was eroding. Production from the major fields had either plateaued or begun declining. New discoveries were failing to keep pace with extraction. Petrobangla’s proven reserves, estimated at approximately 11.9 trillion cubic feet, were being consumed at a rate that implied exhaustion within two to three decades. On the demand side, consumption was growing fast, driven by urbanisation, industrial expansion, and the government’s ambitious growth targets.

Data note: Petrobangla’s 11.9 Tcf proven-reserves figure should be dated explicitly before publication. Reserve estimates are periodically revised and the year of assessment matters for any reader thinking about depletion timelines.

The Power System Master Plan of 2010, and its more consequential 2013 update, formally acknowledged what field engineers had known for some time. Domestic production alone could not sustain the country’s energy needs. LNG imports were identified as a necessary supplement. The implication, though rarely stated so plainly in official documents, was significant: the era of cheap domestic energy was ending, and whatever replaced it would be priced not by Bangladeshi geology but by global commodity markets.

The Option Left on the Table

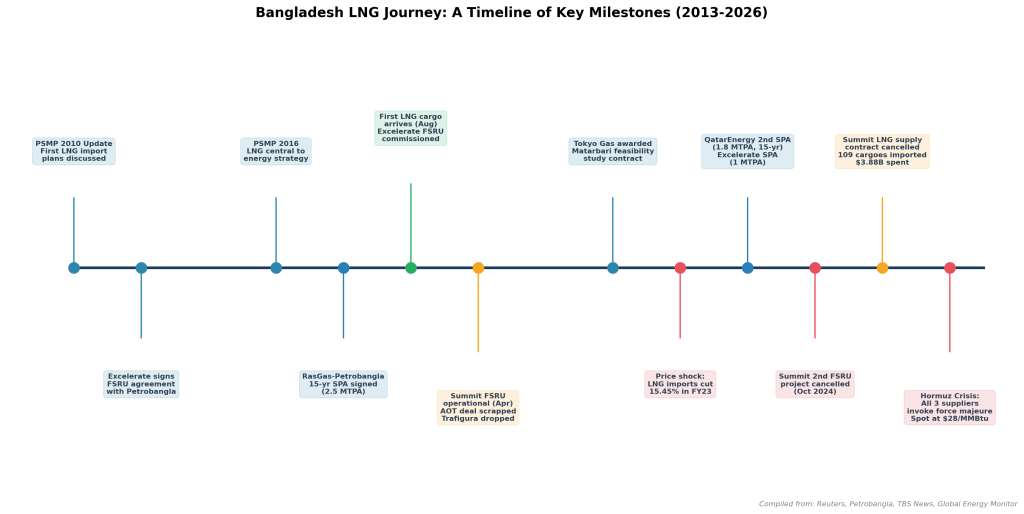

The first serious proposal for LNG importation centred on something permanent. The government identified Matarbari Island in Cox’s Bazar as the site for a large-scale, land-based regasification terminal. The Japan International Cooperation Agency was involved in early planning. Tokyo Gas was later awarded a feasibility study contract in 2021.

The case for a land-based terminal was not complicated. It would have a longer operational lifespan, between 30 and 40 years compared with 15 to 20 for a floating unit. It would carry meaningfully lower operating costs. Land-based terminals typically run at between $0.30 and $0.60 per MMBtu in operating costs, compared with $0.60 to $1.20 per MMBtu for a chartered FSRU. The difference, compounded across a multi-decade import programme, is substantial. The proposed Matarbari terminal was envisioned with an initial capacity of 7.5 MTPA, expandable to 15 MTPA.

The obstacles were real, though. The capital cost was estimated at $3 to $5 billion, difficult for a government with limited fiscal headroom. Land acquisition in a densely populated coastal area proved politically complex. Environmental assessments raised concerns about the site’s ecology. And the construction timeline of five to seven years from investment decision to first gas was incompatible with the urgency of the supply gap. Bangladesh needed gas in years, not a decade.

The Matarbari terminal has not reached a final investment decision as of 2026. It remains in the planning and feasibility stage, and the Hormuz disruption has cast new uncertainty over its future. Had Bangladesh committed to it in 2016 or 2017, a terminal would be operational today at a fraction of the per-unit cost of the floating infrastructure that now carries the country’s entire import load. That calculation is worth holding in mind as the story continues.

Renting the Infrastructure

Faced with the mismatch between what was needed and what could be built quickly, the government chose speed. Floating Storage and Regasification Units, or FSRUs, are converted LNG carriers fitted with onboard regasification equipment. They can be chartered, moored offshore, and connected to onshore pipeline networks in a fraction of the time required for permanent construction. They are also considerably more expensive over the long run.

The pivotal agreement came in June 2014, when Petrobangla signed a 15-year charter with US-based Excelerate Energy for an FSRU at Moheshkhali Island. The vessel, named Excellence, had a storage capacity of 138,000 cubic metres and a regasification capacity of 500 MMcfd (million standard cubic feet per day), or approximately 3.75 MTPA (million tonnes per annum). A second FSRU was awarded to Summit Group, in partnership with Excelerate Energy, under a 15-year charter signed in August 2017.

Alongside the infrastructure, Bangladesh secured its first long-term supply contract. In September 2017, Petrobangla signed a 15-year Sales and Purchase Agreement, or SPA, with RasGas, a Qatari joint venture later absorbed into QatarEnergy, for 2.5 MTPA of LNG priced on a slope linked to Brent crude oil. It was the anchor commitment of what would become a structurally dependent import programme.

The First Cargoes

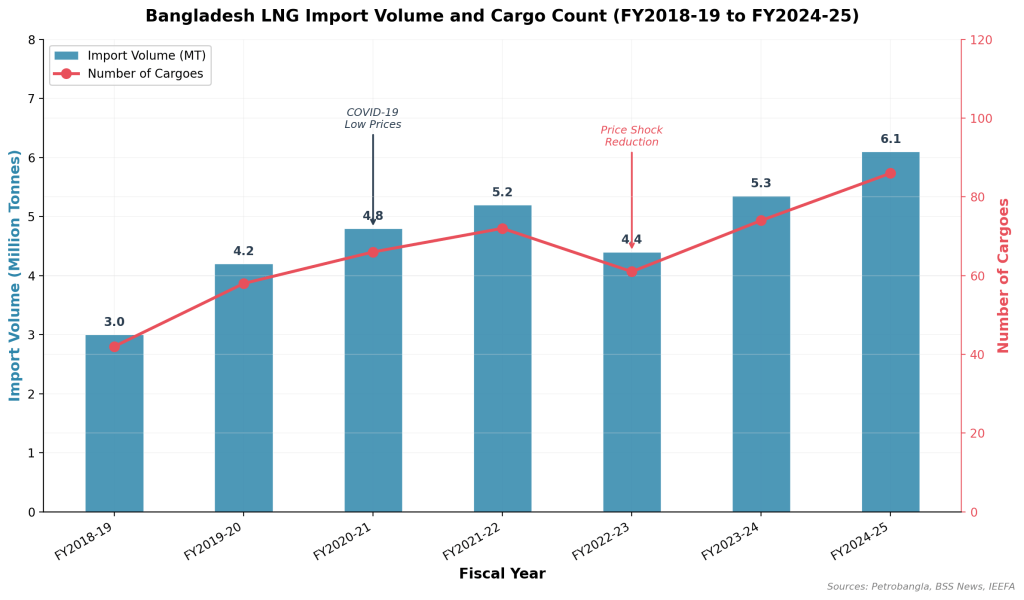

In August 2018, the Excelerate FSRU was commissioned and Bangladesh received its first commercial LNG cargo. The occasion was celebrated as the beginning of a new era of supply diversification. In FY2018-19, Bangladesh imported approximately 3.0 million tonnes of LNG, primarily under the Qatari long-term contract.

By April 2019, the Summit FSRU had begun operations at a separate berth near Moheshkhali, bringing combined regasification capacity to 1,000 MMcfd, or 7.5 MTPA. Bangladesh had the infrastructure. What it did not have was a coherent procurement strategy for volumes beyond the base long-term contract. Negotiations with AOT Energy, a Swiss trading firm, for a medium-term supply deal fell through. A similar arrangement with Trafigura was abandoned. These were early signals of the difficulties Bangladesh would face as a price-sensitive buyer in a market that does not particularly favour smaller importers.

Figure 1: LNG import volumes and cargo counts, FY2018-19 to FY2024-25. The FY2022-23 dip reflects the forced reduction caused by the Russia-Ukraine price shock, not falling demand.

A Narrow Window, Then a Wall

The period from 2020 to 2022 compressed, into two years, the full range of outcomes that global LNG market exposure can produce.

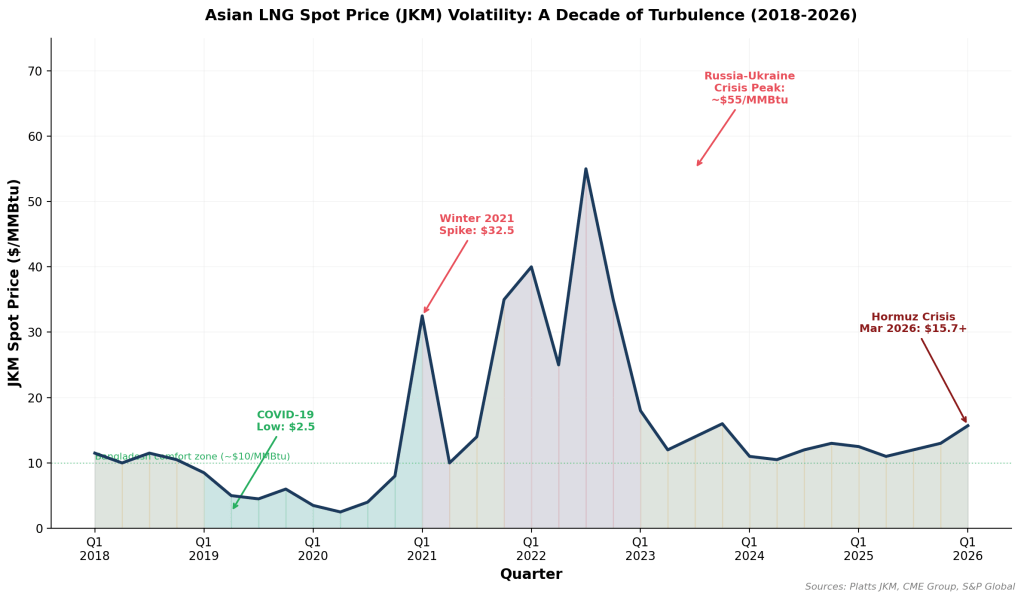

The onset of the COVID-19 pandemic in early 2020 caused a collapse in global energy demand. Asian LNG spot prices, measured by the Japan/Korea Marker or JKM, fell below $2.50 per MMBtu in mid-2020. For Bangladesh, which had been paying rates closer to $6 to $9 per MMBtu under its long-term Qatari contract, this was a genuine opportunity. The government increased spot purchases during this window, and the experience reinforced a perception among some policymakers that the spot market could serve as a cost-effective supplementary channel.

Data note: The precise proportion of total LNG procurement sourced from spot versus long-term contracts during FY2020-21 is not publicly disclosed in detail and would materially strengthen this section. Petrobangla procurement records are the suggested source.

That conclusion proved costly. The global economic recovery, combined with supply-chain disruptions, pushed prices sharply higher in late 2021. The JKM reached $32.50 per MMBtu over the 2021 to 2022 winter. Then Russia invaded Ukraine in February 2022, and Europe entered the global LNG market as an aggressive buyer almost overnight, competing directly with Asian importers for every available cargo. The JKM peaked near $85 per MMBtu in August 2022, more than 34 times the COVID-era low.

Bangladesh could not buy at those prices. The government cancelled and deferred spot cargo purchases. Gas shortages hit households. Rolling power cuts moved across industrial zones. The garment sector, which depends on reliable electricity to run its export floors, absorbed production losses that have not been fully quantified in any published assessment but were described by industry associations as severe.

Data note: BGMEA data on FY2022-23 production losses would convert this section’s most significant claim from qualitative to precise. Even a partial-year revenue estimate would be meaningful for a technical audience.

In FY2022-23, total LNG imports fell by more than 15% compared with the previous year. Not because demand had dropped, but because Bangladesh could not afford what the market was offering. Ember Energy projected in October 2022 that Bangladesh’s spot LNG bill could reach approximately $11 billion between 2022 and 2024. Whether that figure proved accurate has not been reconciled against actual Petrobangla disbursements in any publicly available analysis.

Data note: The Ember $11 billion figure was a forward projection made in October 2022. Reconcile against Bangladesh Bank foreign-exchange disbursement records and Petrobangla annual accounts before using in the final version.

Figure 2: JKM spot price, 2018 to 2026. The COVID-era low, the Russia-Ukraine peak, and the post-Hormuz surge are the three inflection points shaping Bangladesh’s import costs over the period.

“The crisis laid bare the structural flaw in Bangladesh’s procurement approach: a reliance on the spot market that looked sensible in 2020 and looked catastrophic two years later, with no buffer in between.”

Signing in the Aftermath

The 2022 crisis produced a clear institutional response: Bangladesh needed more contracted supply and less exposure to the spot market. Petrobangla moved quickly.

In June 2023, QatarEnergy and Petrobangla signed a second 15-year SPA for 1.5 to 1.8 MTPA, with deliveries starting in early 2026, linked to QatarEnergy’s North Field East expansion. The contract was priced at 13.35% of Brent crude plus $0.30 per MMBtu. At $80 per barrel of Brent, that translates to approximately $11 per MMBtu. At the time of signing, LNG forward swaps for 2026 delivery were trading in the $10 to $12 per MMBtu range, suggesting the pricing was broadly market-rate rather than particularly favourable or punitive. Whether it proves a good deal will depend on where Brent trades across 15 years of deliveries.

In November 2023, Excelerate Energy and Petrobangla signed a 15-year SPA for 0.85 MTPA, rising to 1.0 MTPA from 2028 through 2040. The deal added a degree of supply-source diversification beyond Qatar, as Excelerate draws from a global portfolio. According to S&P Global Commodity Insights, these new contracts were expected to bring Bangladesh’s total contracted volume to approximately 7.2 MTPA by 2027.

Table 1: Bangladesh’s Active Long-Term LNG Supply Contracts (as of early 2026, post-Summit cancellation)

| Contract | Supplier | Volume (MTPA) | Duration | Start Year | Pricing Basis |

| SPA 1 (2017) | QatarEnergy (formerly RasGas) | 2.5 | 15 years | 2018 | Brent-linked slope (est. ~12.65% + $0.50) |

| SPA 2 (2023) | QatarEnergy (NFE expansion) | 1.5 to 1.8 | 15 years | 2026 | 13.35% Brent + $0.30/MMBtu (~$11 at $80 Brent) |

| SPA 3 (2023) | Excelerate Energy | 0.85 to 1.0 | 15 years | 2026 | Brent-linked slope (exact terms undisclosed) |

| Total contracted | ~4.85 to 5.3 |

Note: The Summit LNG supply contract, cancelled in September 2025, has been excluded. SPA 1 pricing is an estimate; exact terms were not publicly disclosed at signing.

The Cutbacks

Progress on long-term contracts was partly offset by decisions made on the infrastructure side that would prove poorly timed. In October 2024, the government cancelled Summit Group’s second FSRU project, which would have added 4.5 MTPA of regasification capacity. The reasons cited included concerns about charter terms, questions about whether additional floating capacity was needed given Matarbari’s continued stall, and fiscal pressures on the government’s overall budget position.

In September 2025, Petrobangla cancelled the Summit LNG supply contract itself, removing a volume buffer from the portfolio and pushing more procurement toward the spot market. In retrospect, these two cancellations narrowed Bangladesh’s contracted coverage precisely in the months before a new supply crisis emerged.

Despite the cutbacks, the volume of imports kept rising. In calendar year 2025, Bangladesh imported approximately 7.3 million tonnes of LNG across 109 cargoes at a cost of roughly $3.88 billion. That was a 19% increase in volume and a 28% increase in expenditure compared with 2024, when 86 cargoes costing $3.02 billion were imported. The demand was not going anywhere.

Data note: Published trade sources give a range of 7.16 to 7.41 MT for 2025 imports, likely reflecting different reporting conventions. Resolve to a single figure from Petrobangla’s official import registry before the final version.

March 2026

On March 1, 2026, Iran closed the Strait of Hormuz. Roughly 20% of global LNG trade passes through the Strait, and a considerably higher proportion of Bangladesh’s contracted supply does so.

QatarEnergy invoked force majeure on March 2. OQ Trading followed on March 5. Excelerate Energy did so on March 6. In the space of five days, Bangladesh’s entire base of contracted LNG supply was suspended. The country was left to buy on a spot market that was moving fast in one direction.

Spot prices had been at approximately $10.73 per MMBtu in late February. Within days they reached $15.70. Bangladesh eventually secured emergency cargoes at $28.28 per MMBtu, approximately 2.6 times the pre-crisis level and more than 11 times the COVID-era lows that had once seemed to validate the spot market as a sensible supplementary channel.

Data note: The specific JKM price trajectory ($10.73, $15.70, and $28.28 per MMBtu) and the force majeure dates (March 2, 5, and 6) are the most operationally significant figures in Part 1 and are currently uncited. Pin each to a primary or wire-service source: Platts/S&P Global LNG Daily, ICIS LNG Edge, or Reuters LNG coverage from March 2026.

The closure made visible something that years of incremental decisions had obscured. Bangladesh’s contracts were concentrated in a single geographic corridor. Its floating terminals provided no buffer storage. Its domestic production was insufficient to compensate for even a partial supply disruption. Its power generation was too dependent on gas to switch, at scale, to anything else at short notice. Each of those weaknesses had been noted, in isolation, at various points over the previous decade. In March 2026 they arrived together, and Bangladesh ended up exactly where the international analysts had placed it: among the most exposed countries in the world, rationing fuel, closing universities, and buying emergency spot cargoes at prices that would have been unthinkable a month earlier.

The businesses that spent years complaining about gas pressure were measuring a symptom. What the Hormuz closure measured was the underlying condition. How Bangladesh built that condition, and whether there is a way out of it, is what this series examines. Part 2 starts with the numbers.

Figure 3: Key Milestones in Bangladesh’s LNG Journey, 2010 to 2026

Coming Up in Part 2

Part 2, “Pressure Points” moves from the timeline to the underlying logic. It traces the decline curve of domestic gas production in detail, examines what the choice between long-term contracts and spot exposure actually costs Bangladesh across different price scenarios, looks at the geographic concentration of supply and what the Hormuz closure exposed, and lays out the full financial picture: the $18 billion cumulative import bill, the subsidy burden, and the foreign exchange drain that now sits behind every other economic policy decision the government makes. The question it tries to answer is specific: not how Bangladesh got here, but whether there is a way out.