22 2 月

Bangladesh has had “sustainable finance” as a policy conversation for years. What has been rarer is a repeatable execution model, one that helps multiple financial institutions move from ambition to market-ready thematic instruments, with credible governance, verifiable proceeds tracking, and reporting that can withstand investor scrutiny. Recent market activity, including BRAC Bank’s planned BDT 1,000 crore social subordinated bond, signals that the conversation is shifting from intent to execution. More importantly, it points to an emerging pipeline opportunity where multiple banks can issue credible thematic instruments if the underlying governance, controls, and investor-facing disclosures are made repeatable. (The Daily Star)

This is where technical assistance can become catalytic at a market level. Inspira Advisory & Consulting Limited, in collaboration with Water.org, is supporting a growing pipeline of social, green, and sustainability-linked bond issuances with several commercial banks in Bangladesh, across both BDT-denominated and USD-denominated structures. The objective is not to “write a framework” for a single transaction; it is to strengthen the operating systems behind labelled issuance so banks can execute reliably, attract the right investors, and build confidence through consistent post-issuance reporting.

Why BDT and USD thematic bonds matter, and why execution sequencing is the real barrier

Across emerging markets, the most scalable sustainable finance stories are increasingly local-currency stories, because domestic balance sheets lend in domestic currency. At the same time, USD thematic issuance can unlock deeper pools of capital and longer tenors, but it also raises the bar on disclosure, governance signals, and investor expectations. For Bangladesh, the opportunity is therefore twofold: strengthen the domestic BDT pipeline and prepare select issuers for USD markets through a sequencing approach that makes frameworks, controls, and reporting “exportable” to global investors.

BRAC Bank’s instrument is also subordinated, designed to support Tier-II capital under Basel III. In plain terms, that means it sits below senior obligations in the capital structure and is recognized as regulatory capital subject to specific rules on subordination, maturity, and loss-absorption characteristics. This matters for investors because it changes the risk profile and therefore demands clearer disclosure and stronger confidence in the issuer’s governance. (The Business Standard)

A global market that is scaling, and a regional gap Bangladesh can close

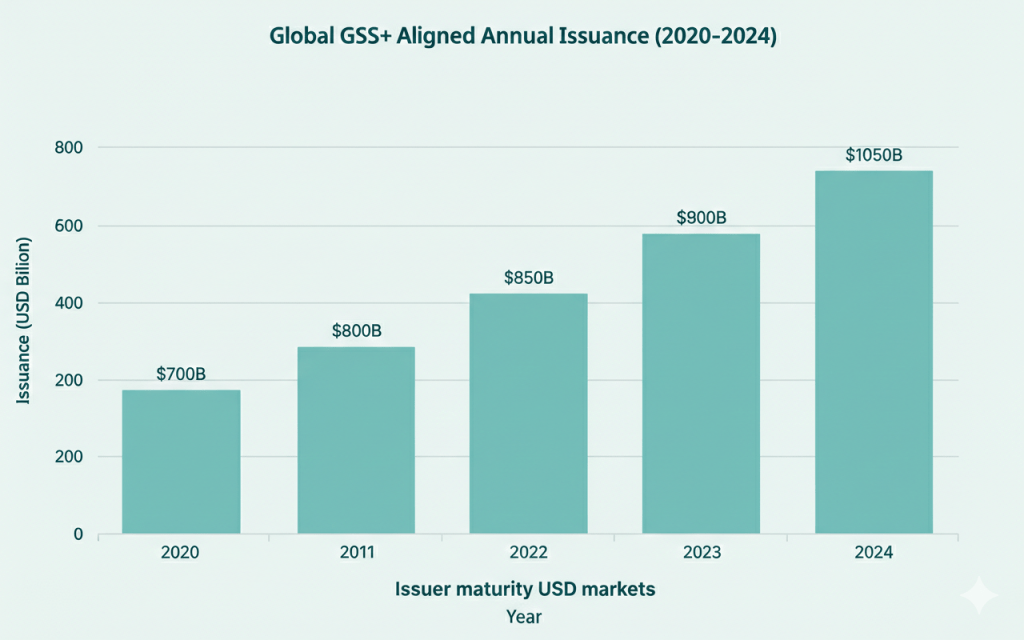

The broader thematic debt market has been expanding quickly. Climate Bonds’ “Global State of the Market 2024” reports USD 1.05 trillion in aligned GSS+ deals priced in 2024, a record year, and notes that 2024 aligned volume exceeded the 2023 figure (USD 946.9bn).

FIGURE 1: Global GSS+ aligned annual issuance (2020–2024)

But even as global aligned issuance scales, Bangladesh remains early in the regional thematic-bond curve, particularly in building a repeat-issuer pipeline supported by standardized playbooks, credible external reviews, and post-issuance reporting discipline. Peer markets in South and Southeast Asia have already built multi-billion-dollar pipelines across green, social, and sustainability themes. Bangladesh’s next step is to move from “landmark transactions” to repeatable issuance capacity, especially among banks that can mobilize domestic savings at scale and, where appropriate, access USD markets without weakening credibility.

If you consider the local regulatory context around thematic bonds, keep it factual and framed as “evolving rules”. Bangladesh’s regulator has publicly discussed proposed updates to thematic bond provisions, including expanding categories and updating requirements. (The Business Standard)

FIGURE 2: Bangladesh vs regional peers (indicative cumulative GSS+ issuance)

What makes a bank-led thematic bond replicable: the control system behind it

ICMA’s Social Bond Principles are process guidelines built around four core components: Use of Proceeds, Process for Project Evaluation and Selection, Management of Proceeds, and Reporting. Their real contribution is not marketing language; it is a discipline of disclosure that lets investors understand how money moves from issuance to impact. This matters because, for banks building thematic pipelines, the central question is not whether a label can be claimed. The question is whether internal controls, tracking systems, and reporting routines can be operated consistently across products, branches, and years. (ICMA)

For example, BRAC Bank’s Social Bond Framework makes the bond’s social intent operational by specifying eligible categories and a governance approach for selection, allocation tracking, and reporting. The framework sets out how proceeds may be applied to social categories (such as access to finance and essential services), how refinancing is treated, and how allocation reporting will be produced. (brackweb.s3.ap-southeast-1.amazonaws.com)

| SBP 2025 core component | What ICMA expects | “Bank controls” that make it real |

| 1) Use of Proceeds | Define eligible social categories; commit proceeds to them | Eligibility taxonomy; product/portfolio tagging; exclusion rules |

| 2) Project Evaluation & Selection | Explain how projects/assets are chosen | Governance committee; approval memos; eligibility checklists; audit trail |

| 3) Management of Proceeds | Track, allocate, and manage unallocated proceeds transparently | Segregated tracking; internal ledger; allocation register; reconciliation |

| 4) Reporting | Publish allocation and impact reporting (typically annually) | KPI library; data QA; reporting templates; assurance-ready evidence |

TABLE 1: How SBP translates into bank controls

When you read the framework through an investor lens, the deeper story becomes clear: this is an attempt to standardize credibility. In markets where thematic bonds are still emerging, the cost of credibility can be high. Issuers must build internal tagging systems, define eligibility screens, train teams, establish monitoring routines, and prepare reporting that can survive scrutiny. That fixed-cost barrier is exactly why many countries use catalytic support mechanisms (including grants for external reviews) to accelerate early market formation. Singapore’s MAS, for instance, has a Sustainable Bond Grant Scheme that offsets eligible external review expenses (up to a defined cap), explicitly to support credible issuance practices. Hong Kong’s HKMA has similarly operaat subsidizes eligible issuance and external review costs and has been extended and expanded over time. (Monetary Authority of Singapore)

Where Inspira and Water.org create leverage: technical assistance that makes issuance repeatable

In practice, Inspira’s collaboration with Water.org is designed around one simple goal: make labelled issuance operational, not aspirational. The technical assistance is therefore built as a repeatable system that can be tailored across banks and across instrument types, including use of proceeds bonds such as social and green and performance based instruments such as sustainability linked bonds, while keeping the credibility expectations constant. Those expectations are shaped by widely used market guidance on use of proceeds bonds and sustainability linked bonds. (ICMA Social Bond Principles, June 2025, ICMA Green Bond Principles, June 2025, ICMA Sustainability Linked Bond Principles, June 2024)

This is also why the programme goes beyond documentation. Where relevant, it includes investor mapping, matchmaking, and deal facilitation support so issuers can understand investor appetite, align issuance features with realistic pricing expectations, and engage the right counterparties at the right stage.

In practice, Inspira’s technical assistance, facilitated through Water.org, clusters around five recurring workstreams that can be tailored to each bank’s instrument type, risk profile, and market route.

(1) SPO and assurance readiness, so external review becomes a quality gate, not a delay

A recurring bottleneck for first time issuers is that external review preparation is treated as narrative drafting, when reviewers actually need testable evidence. Inspira supports participating banks by shaping the engagement scope, tightening the technical annexes, and packaging inputs in a form that enables reviewers to test alignment efficiently. This includes clarifying eligible categories, defining exclusion logic, and documenting how proceeds management will work in practice, so the external review can assess substance rather than intent. The approach is consistent with how ICMA frames external review and transparency expectations as part of credible market practice for use of proceeds bonds. (ICMA SBP, June 2025, ICMA Principles Guidance Handbook, June 2025)

In parallel, the TA is structured to anticipate post issuance assurance from day one. Rather than leaving allocation auditability and impact verification as an afterthought, banks are supported to define what will be audited, what evidence will be retained, and how reporting outputs will be produced annually, so assurance becomes routine rather than a scramble.

(2) Impact monitoring and reporting design, turning eligible categories into reportable outcomes

A common weakness in early stage thematic issuances is that “eligible categories” are clear, but reporting becomes vague once proceeds begin to flow through real portfolios. Inspira addresses that gap by building a bond level monitoring and reporting spine that specifies how data is captured, verified, consolidated, and translated into allocation and impact tables that can be repeated year after year. This is aligned with the reporting emphasis embedded in the core components of the Social Bond Principles and related reporting guidance. (ICMA SBP, June 2025, ICMA Harmonised Framework for Impact Reporting for Social Bonds, June 2025)

Where the pipeline includes sustainability linked structures, the logic shifts from category eligibility to KPI design and target credibility. In those cases, the TA focuses on KPI selection discipline, target calibration, disclosure readiness, and the evidence plan that will support verification of performance against targets. (ICMA SLBP, June 2024)

(3) Institutional capacity building, making thematic execution business as usual

Even the best framework fails quietly if branch teams interpret eligibility differently across products, or if risk teams apply inconsistent judgement across regions. The TA therefore supports internal readiness across product, risk, treasury, and relevant business lines, with learning content that is adapted to the bank’s portfolio reality and the thematic focus of the instrument. The nuance here is practical: the objective is not general ESG training, it is consistent execution, meaning staff can identify eligible lending, apply the same eligibility logic, retain the right evidence, and feed reporting systems without friction.

Beyond workshops, Inspira supports banks to translate learning into execution tools that reduce variability, including appraisal guidance, decision checklists, portfolio tagging logic, and staff facing job aids. This is often where credibility is won or lost, because consistency across a bank’s footprint is what ultimately determines whether reporting stays defensible after issuance.

(4) Customer and market enablers, ensuring proceeds can actually be deployed

A framework does not deploy capital, products, partners, and borrower awareness do. So the TA often includes customer and partner enablement materials that reduce information barriers and standardize messaging at branch and partner levels. This can include borrower friendly guides, FAQs, visual job aids, and simple explainer content that helps relationship managers communicate eligibility and documentation requirements clearly.

Where Water.org is involved in strengthening thematic lending pipelines linked to water and sanitation outcomes, the enablement layer also helps ensure that demand creation and partner engagement remain consistent with the bond narrative, and that lending records remain clean and verifiable for reporting.

(5) Knowledge, replication, and investor engagement support, so the first becomes a template

The highest value outcome of technical assistance is not one successful issuance, it is a model that can be repeated across issuances and across institutions. That is why this collaboration includes structured learning documentation and replication support, capturing what worked, what created friction, and what should be standardized for the next issuance cycle.

Where relevant, the programme also supports investor mapping and engagement logic so banks can align instrument design and disclosure depth with investor expectations, and approach the market with realistic sequencing. This is especially important when a pipeline includes USD issuance pathways, where governance signals, disclosure quality, and reporting readiness are tested more aggressively by global investors.

| What investors / regulators need to see | What Inspira’s TA delivered in practice | Why it matters |

| “Is this bond aligned and independently reviewable?” | SPO engagement scope + technical annexes + organized evidence pack | Speeds review, reduces ambiguity, strengthens credibility |

| “Can proceeds be audited and traced?” | Audit/assurance documentation structure and reporting readiness inputs | Makes allocation controls verifiable post-issuance |

| “How will impact be measured annually?” | Bond-level M&E framework + WASH indicators + data verification logic | Enables consistent, comparable reporting across years |

| “Can staff execute eligibility consistently?” | Training + toolkits + WASH appraisal checklists for retail/SME/risk teams | Prevents drift between framework and frontline decisions |

| “Will capital actually deploy into real borrowers?” | Borrower-facing guides + partner messaging support + demand activation inputs | Improves uptake and reduces operational friction |

| “Is this a one-off or a replicable model?” | Knowledge capture + investor positioning support + innovation pathway inputs | Helps turn a ‘first’ into a market template |

TABLE 2: What investors ask vs. what TA delivered

The bigger precedent: moving from one-off issuance to a bank-led pipeline

Bangladesh already has a debt securities architecture that is moving toward clearer expectations for labelled instruments, including proceeds governance, disclosures, and reporting discipline. The direction of travel is visible in public reporting on proposed amendments to the Debt Securities Rules that would expand sustainable bond definitions and update provisions for thematic issuance, signalling that regulators want the market to mature beyond isolated transactions. (The Business Standard)

The next step is therefore not to lower standards, but to make standards easier to execute. In practical terms, that means translating “principles” into repeatable operating routines: eligibility screens that hold up under scrutiny, internal tagging that can be reconciled, evidence retention that makes audits straightforward, and reporting templates that can be reproduced annually without reinventing the process each time. That is the difference between a landmark issuance and a credible pipeline.

This is also why the current moment is best read as a pipeline building story rather than a single product story. Bangladesh is scheduled to graduate from the UN Least Developed Country category on 24 November 2026, a milestone that increases the premium on credible, market based financing channels as preference regimes and investor expectations evolve. (United Nations) Public reporting also shows that the government has recently asked the UN to consider a three year deferral, which underlines how sensitive the transition period is and why preparation quality matters regardless of the final timeline. (The Financial Express)

Within that context, the precedent is not any single bank’s label. The precedent is whether Bangladesh can build a repeat issuer pipeline where multiple banks can issue thematic instruments that look consistent to investors, behave consistently in proceeds management, and report consistently after issuance. This is exactly where the Inspira and Water.org collaboration becomes market shaping. The technical assistance reduces the fixed cost of credibility by building reusable systems, so each new issuance starts from a stronger baseline instead of starting from scratch.

The practical lesson is straightforward. A thematic bond is not only a funding instrument. It is a governance commitment that must remain credible to investors, regulators, and the public long after the issuance date.