20 8 月

Key Takeaways

- Severe Import Dependence: Bangladesh imports over 90% of its medical equipment. Local producers meet only 8% of demand, with just 4 large-scale factories in operation.

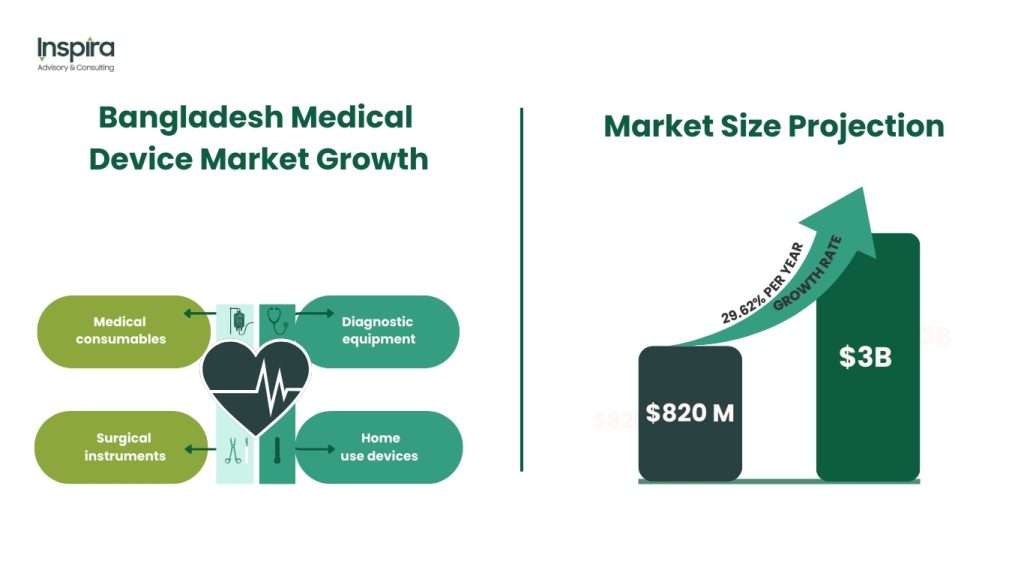

- Huge Market Growth: The medical equipment market is valued at $820M now and will reach $3B by 2030, projected to grow at 29.62% CAGR.

- Strong Cost Advantage: Labor costs are far lower than China ($1,301/month) and India ($734/month). Bangladesh’s average is $370/month. Combined with expertise in textiles and pharmaceuticals, this creates a strong base for device manufacturing.

- High-Potential Segments: Home-use devices (thermometers, BP monitors, glucometers, oximeters) and medical consumables (syringes, blood bags, sterilizers) have rising demand and relatively simple production needs.

- Government Incentives: Investors get lower import duties, 50% tax exemption on export income, and 0% VAT on exports. Post-COVID, PPE and sanitizer inputs received duty waivers.

- Quality & Certification Gap: The main barrier is quality control. Without strong domestic testing and certification institutions, scaling exports and trust in local products will be limited.

- Export Potential: With its cost edge and government support, Bangladesh targets $500M+ medical device exports by 2030, especially to regional markets under trade agreements.

Bangladesh’s medical equipment sector presents a compelling case for import substitution, with the domestic market valued at US$820 million and projected to reach US$3 billion by 2030.The market is projected to experience a 29.62% growth of Compound Annual Growth Rate (CAGR). This sector offers significant opportunities for local manufacturers to reduce the country’s heavy reliance on imports while capturing substantial market share.

Bangladesh currently imports the vast majority of its medical equipment needs, with existing local manufacturers serving only 8% of the domestic market. Approximately 15-20 manufacturing facilities operate in the country, with only four considered large-scale operations. This heavy import dependency creates both a challenge and an opportunity – while it indicates market demand, it also reveals untapped potential for local production.

The medical equipment landscape spans diverse categories including medical consumables (disposable syringes, needles, blood bags), surgical instruments, diagnostic equipment, and home health monitoring devices. The growing demand is driven by expanding healthcare infrastructure, increasing prevalence of non-communicable diseases, and rising health consciousness among Bangladesh’s growing middle class.

Competitive Manufacturing Advantages

Bangladesh offers several compelling advantages for medical device manufacturing. Manufacturing and non-manufacturing wages are significantly competitive compared to regional peers like China (US$1,301) and India (US$734), with Bangladesh’s average non-manufacturing wage at US$370 per month. This cost advantage, combined with the country’s established manufacturing expertise in textiles and pharmaceuticals, creates a strong foundation for medical device production.

The government has recognized this potential and offers attractive investment incentives. These include concessional import duties under SRO 11/AN/2021/06/Customs for raw materials in medical equipment manufacturing, post-COVID duty waivers for PPE and sanitizer materials, and 50% tax exemption on export income with 0% VAT on shipped goods.

Market Opportunities and Growth Segments

The direct-to-consumer segment represents a particularly promising opportunity that has been historically overlooked. Rising health consciousness and increasing complexity of non-communicable diseases are driving demand for low-risk medical devices and home health monitoring equipment. Middle-income families are increasingly purchasing digital thermometers, blood pressure monitors, glucometers, and pulse oximeters as household staples.

Medical consumables production offers another high-potential area, given Bangladesh’s existing capabilities in related manufacturing sectors. Items like disposable safety syringes, blood collection tubes, and surgical sterilizers have consistent demand and relatively straightforward production requirements

Competition context and benchmarks

Positioning needs hard external benchmarks. Malaysia exported about US$4.2 billion of medical devices in 2022 and is a regional hub for catheters, gloves, and single‑use devices, supported by a deep supplier base and med‑tech infrastructure (MIDA/BMI, 2024). Türkiye has scaled exports to roughly US$1.25 billion by 2023, helped by localization policies and a growing contract‑manufacturing base (Gün Law, 2025). Vietnam remains highly import‑dependent for its domestic market but is expanding manufacturing; for HS 9018.90 alone, it exported about US$366 million in 2023 (WITS, 2025; ITA, 2024). Note that figures differ by HS coverage and industry definitions; use a consistent taxonomy when setting Bangladesh targets.

Strategic Implementation Framework

Successful import substitution requires a shift from import-dependent to locally produced manufacturing. This involves establishing completely built-up (CBU) or semi-knocked down (SKD) manufacturing processes rather than completely knocked down (CKD) assembly operations that still rely heavily on imported components.

Quality control and certification remain critical challenges that must be addressed. While top-tier manufacturers already produce WHO-compliant medical equipment, there is a need for unified and standardized products that can only be ensured by third-party domestic institutions for product testing and certification. This presents another investment opportunity in establishing quality control laboratories.

Export Potential and Regional Markets

Beyond import substitution, Bangladesh’s cost advantages and improving bioequivalence testing infrastructure position the country to leverage EPZs/EZs for low-risk device production. The government aims to elevate medical equipment exports to $500M+ by 2030, targeting regional markets under preferential trade agreements.

Demand‑side risks to a 29.62% CAGR

The 29.62% CAGR assumption should be stressed‑tested against financing and procurement frictions. Out‑of‑pocket spending remains among the world’s highest, with OOP at about 73% of total health expenditure in 2021, implying limited headroom for capex‑heavy adoption without financing mechanisms (CPD, 2024). Formal insurance coverage is extremely low; a BDHS‑based 2025 analysis finds only 0.3% of women report any health insurance, which undermines steady demand for higher‑end diagnostics (Al Fidah et al., 2025). Public procurement bottlenecks also constrain uptake: a BPPA post‑review shows 40% single‑bid awards at CMSD in FY2023‑24, and earlier audits documented unused equipment and pricing anomalies, signaling execution risk even when budgets exist (The Financial Express, 2025; The Daily Star, 2023). These realities argue for calibrated growth scenarios, patient financing or leasing for providers, and procurement reforms alongside local production.

Bangladesh’s medical device sector represents a significant import substitution opportunity driven by strong domestic demand, competitive manufacturing costs, and supportive government policies. Success requires strategic focus on high-demand segments like consumables and home health devices, combined with investments in quality infrastructure and certification capabilities. With proper execution, local manufacturers can capture substantial market share while building export capabilities for regional expansion.

The medical equipment sector’s projected growth to US$3 billion by 2030 represents not just an import substitution opportunity, but a pathway to establishing Bangladesh as a regional medical device manufacturing hub.

Reference:

- Al Fidah, M. F., Islam, M. R., & Mohammad, S. (2025). Understanding health insurance coverage and its socio-demographic associations among women in Bangladesh: Evidence from the 2022 BDHS. Global Health Economics and Sustainability.

- Center for Policy Dialogue. (2024). Health Budget of Bangladesh: Optimising resources for improved health outcomes. https://tinyurl.com/494fmr8f

- Gün + Partners. (2025). Türkiye’s medicines and medical devices sectors: Current status and evolving dynamics.

- International Trade Administration. (2024). Vietnam—Healthcare.

- https://www.mida.gov.my/mida-news/bmi-malaysias-medical-devices-market-to-benefit-from-health-spending-in-2024/

- https://www.thedailystar.net/opinion/editorial/news/procurement-system-shambles-3357646

- https://thefinancialexpress.com.bd/trade/single-bid-marks-40pc-of-contracts

- World Bank WITS. (2025). Vietnam exports of HS 9018.90 instruments and appliances (2023)