24 Mar

The three structural weaknesses in Bangladesh’s energy system, and what the Hormuz crisis did to each of them.

When researchers at the Centre for Global Development ranked countries by their exposure to the Iran war’s energy disruption in March 2026, they measured three things: how dependent a country was on imported fuel, how much foreign exchange it had available to pay for it, and how heavily indebted it already was. Bangladesh appeared near the top of all three. Al Jazeera named it among the countries facing the gravest risks. The Straits Times placed Bangladesh alongside South Korea and Indonesia in a group of Asian nations pivoting to coal because LNG had become, in the words of one Rystad Energy analyst, “simply unaffordable.” The World Economic Forum logged university closures and fuel rationing as headline consequences of the crisis.

The coverage was accurate. What it did not explain was the mechanism: why Bangladesh was exposed to this degree, and why a country that had been signing long-term LNG contracts for years arrived at March 2026 with so little room to absorb a shock. The answer is not a single decision or a single policy failure. It is three structural conditions, each of which was visible long before the crisis, and none of which was resolved.

Part 1 of this series traced the history: how Bangladesh moved from near-total domestic gas self-sufficiency to structural LNG dependency across a decade. Part 2 is about what that dependency looks like now, in numbers. The picture is more specific, and more uncomfortable, than the international headlines suggested.

| KEY FINDINGS — PART 2 | |

| Production decline | Domestic gas output has fallen from a peak of roughly 2,750 MMcfd to approximately 1,950 MMcfd in FY2024-25, a decline of nearly 30% in under a decade. The Ramboll/EQMS report estimates reserves will be exhausted by 2038 without significant new discoveries. |

| The supply gap | Bangladesh’s total gas demand of roughly 3,800 to 4,000 MMcfd cannot be met. Even with LNG, the country runs a shortfall of over 1,000 MMcfd that does not show up in import statistics: it shows up in factory rationing, curtailed fertiliser output, and load-shedding. |

| The spot market exposure | Roughly 29 to 35% of LNG cargoes are sourced from the spot market, depending on the year. Most major LNG-importing nations treat 20 to 25% as a ceiling. Petrobangla’s projected annual deficit from subsidised domestic gas sales was approximately $690 million in 2025. |

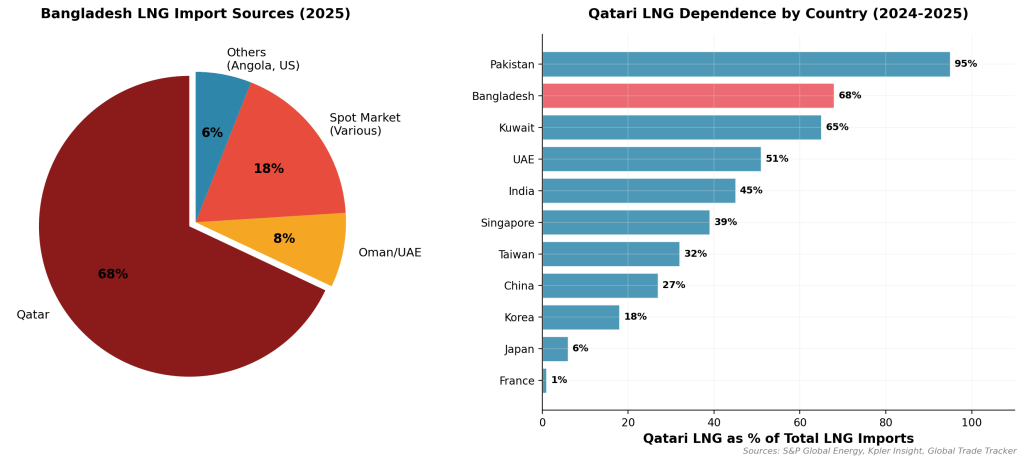

| Geographic concentration | Between 68% and 75% of Bangladesh’s LNG comes from Qatar. Add Oman, and the Middle Eastern share exceeds 85% of contracted supply. Every cargo from Qatar must transit the Strait of Hormuz. |

| The compounding effect | The three vulnerabilities do not operate independently. Declining domestic production forces more LNG purchases. More spot LNG means more price exposure. Geographic concentration and zero strategic storage mean that when a supply corridor closes, there is no fallback. |

The Anatomy of Bangladesh’s LNG Dependency

What’s Left in the Ground

The most fundamental problem is one that no contract renegotiation or infrastructure project can solve in the short term: Bangladesh’s domestic gas fields are running dry, and they are doing so faster than official projections have tended to acknowledge.

Production peaked in the mid-2010s at approximately 2,750 MMcfd and has been declining ever since. Bibiyana, the country’s flagship field, dropped from around 1,223 MMcfd in FY2020 to roughly 1,032 MMcfd by FY2024, a fall of 16% in four years from the country’s single most important gas source. Across all fields, domestic output fell by more than 8% in the 16 months to December 2025 alone, an acceleration that analysts project will steepen to a 12% compound annual decline between 2024 and 2028 as the major fields enter their terminal phase.

Data note: The 12% CAGR decline projection (2024-2028) requires attribution to a named analyst or report before publication. If derived from Petrobangla production data, state this explicitly.

It is worth being precise about who operates what is left. Chevron, the US energy major, accounts for approximately 60% of Bangladesh’s total domestic gas output. Petrobangla’s own production arm covers most of the remainder, with Tullow at roughly 2%. That concentration means Bangladesh’s domestic gas future is substantially dependent on the investment decisions of a single foreign operator, a fact that receives little attention in the energy policy debate.

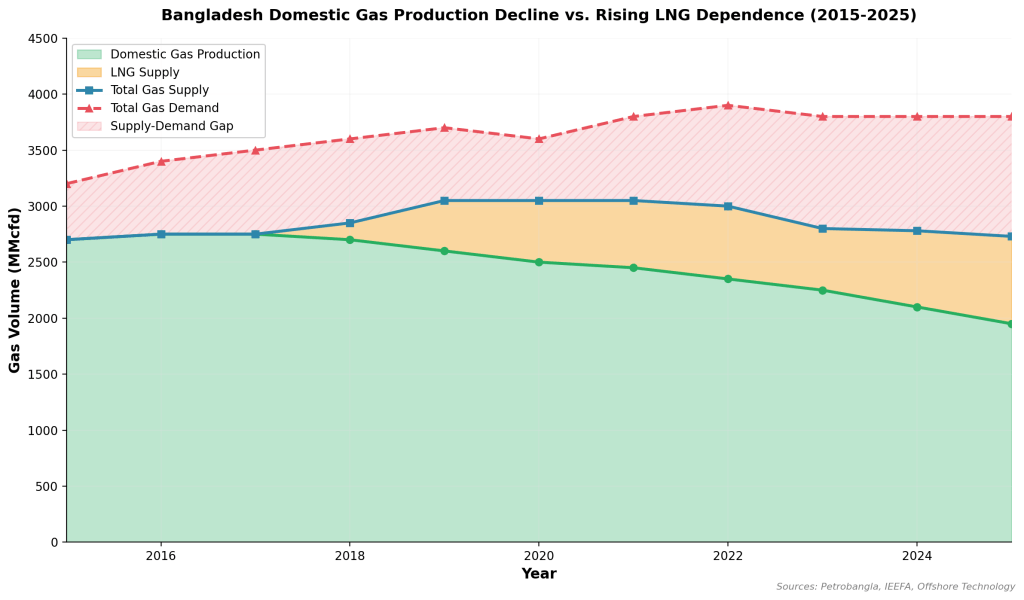

The consequence of this decline is a structural supply-demand gap that LNG has been partially filling for seven years. Total gas demand has remained relatively stable at 3,800 to 4,000 MMcfd, but the domestic share has shrunk relentlessly. In FY2024-25, the gap between what Bangladesh could produce and what its economy required was over 1,000 MMcfd. Crucially, even that figure understates the true shortfall: much of the unmet demand simply goes unfulfilled. It does not show up in import statistics. It shows up in rationed gas for factories, curtailed fertiliser output, and rolling load-shedding. The Ramboll and EQMS Consulting report, prepared for international lenders, estimated that without significant new discoveries, reserves could be exhausted by 2038. Bangladesh’s gas exploration budget has received minimal allocations for most of the past two decades.

Table 1: Bangladesh Gas Supply-Demand Balance, FY2020-21 to FY2024-25

| Parameter | FY20-21 | FY21-22 | FY22-23 | FY23-24 | FY24-25 |

| Domestic production (MMcfd) | 2,500 | 2,350 | 2,250 | 2,100 | 1,950 |

| LNG supply (MMcfd equiv.) | 550 | 650 | 550 | 680 | 780 |

| Total gas supply (MMcfd) | 3,050 | 3,000 | 2,800 | 2,780 | 2,730 |

| Estimated demand (MMcfd) | 3,800 | 3,900 | 3,800 | 3,800 | 3,800 |

| Supply-demand gap (MMcfd) | 750 | 900 | 1,000 | 1,020 | 1,070 |

Sources: Petrobangla production data, IEEFA, Gas Outlook. Demand estimates reflect total gas requirements including unmet demand; they are not import or consumption figures.

Figure 1: Bangladesh gas supply-demand balance, 2015 to 2025.

The Price of Flexibility

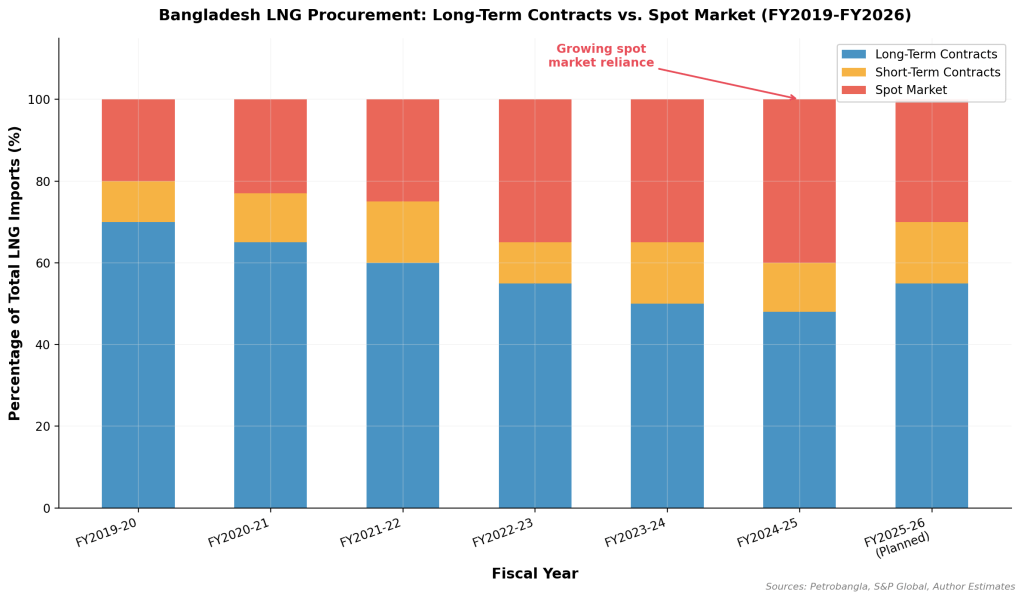

Against the backdrop of domestic decline, Bangladesh has had to buy more LNG each year. The way it buys that LNG has compounded the original vulnerability considerably.

Petrobangla’s procurement operates across three layers: long-term supply agreements, short-term contracts, and the open spot market. In theory, the balance between them provides flexibility and cost management. In practice, the spot market share has repeatedly become a source of crisis rather than a buffer against one.

The temptation of spot purchasing is not hard to understand. When the COVID-19 pandemic collapsed global demand in 2020, JKM spot prices fell below $2.50 per MMBtu, a fraction of the approximately $8 to $10 per MMBtu cost of Bangladesh’s Qatari long-term contract. Buying spot made obvious sense. The problem is that the logic inverts without warning. In 2022, as Europe scrambled to replace Russian pipeline gas, the same spot market surged to $85 per MMBtu. Bangladesh, with a sovereign credit rating of Ba3/BB- and limited foreign exchange purchasing power, was simply outbid. Spot cargoes went to wealthier, higher-rated buyers in Europe and Northeast Asia, and Bangladesh was left to manage shortages at home.

For FY2025-26, Petrobangla’s own procurement plan shows 33 spot cargoes out of a planned 115 total, or approximately 29% of imports from the open market. In peak demand months of 2025, the share ran higher: RPGCL, Petrobangla’s LNG procurement subsidiary, bought 35 spot cargoes in January to August 2025, compared with 21 in the same period a year earlier. Most major LNG-importing nations treat a 20 to 25% spot ceiling as a risk management threshold. Bangladesh has consistently exceeded it.

Data note: The article’s original figure of ‘40% spot in FY2024-25’ is higher than what Petrobangla’s published procurement plans show for FY2025-26 (29%). Reconcile this against RPGCL cargo-level data before publication. The figures may reflect different base periods or definitions of ‘spot.’

Figure 2: LNG procurement breakdown by contract type, 2018 to 2025.

“When global demand surges or supply is disrupted, spot prices can escalate to multiples of long-term contract prices within weeks. Bangladesh, as a relatively small, sub-investment-grade buyer, is routinely among the last served.”

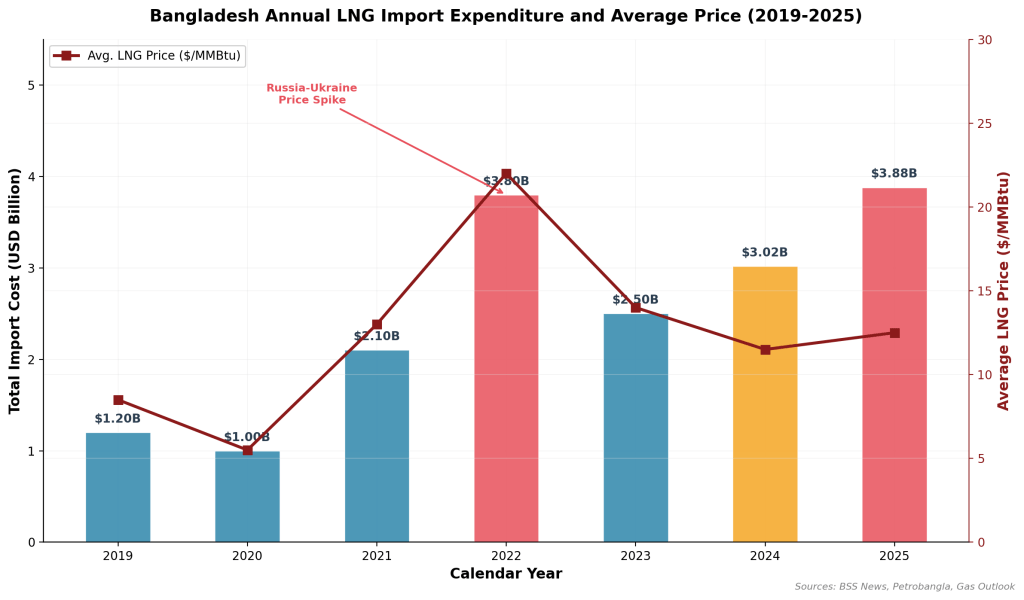

The financial consequences accumulate steadily and are now large enough to have caught the attention of international lenders. From 2018 to 2025, Bangladesh spent a cumulative figure approaching $15 billion on LNG imports, a sum that has grown from roughly $800 million in the first partial year of imports to $3.88 billion in 2025 alone. The annual bill has more than quadrupled in six years.

Data note: The article’s original cumulative figure of $18 billion covers ‘2018 to 2025’ but the supporting table’s data rows begin in 2019. The table below restates the cumulative from FY2018-19, which gives a lower figure. Verify the precise cumulative total against Petrobangla annual accounts before publishing either number. The FDI comparison (‘exceeds total FDI inflows over the same period’) is a powerful claim that requires an actual FDI figure to be defensible.

Table 2: Bangladesh LNG Import Volumes and Costs, FY2018-19 to FY2024-25

| Year | Cargoes | Volume (MT) | Cost (USD bn) | Avg. Price ($/MMBtu) | Spot share (est.) |

| 2018-19 | ~28 | ~2.0 | ~0.8 | ~9.0 | Low (~5%) |

| 2019-20 | ~42 | ~3.0 | ~1.2 | ~8.5 | ~10% |

| 2020-21 | ~58 | ~4.2 | ~1.0 | ~5.5 | ~25% |

| 2021-22 | ~66 | ~4.8 | ~2.1 | ~13.0 | ~30% |

| 2022-23 | ~61 | ~4.4 | ~2.5 | ~14.0 | ~25% |

| 2023-24 | 86 | ~6.0 | 3.02 | ~11.5 | ~28% |

| 2024-25 | 109 | ~7.3 * | 3.88 | ~12.5 | ~29-35% |

| Cumulative 2018-25 | ~450 | ~31.7 | ~$14.5 bn ** |

Sources: BSS News, Petrobangla, Gas Outlook, IEEFA. * 2024-25 volume from Gas Outlook (range: 7.16-7.41 MT; reconcile to single figure). ** Cumulative restated from FY2018-19; differs from $18bn figure in some published analyses.

The government’s response to rising import costs, subsidising domestic gas prices to shield consumers and industry from the true cost of imports, has created a separate fiscal problem running alongside the supply one. Petrobangla sells gas to end users at somewhere between three and five dollars per MMBtu while buying it at eleven to thirteen dollars. The gap, multiplied across a growing import volume, produced a projected Petrobangla operating deficit of approximately $690 million in 2025 alone. Added to that is the cost of the floating regasification infrastructure itself: analysts estimate the two FSRUs have cost roughly BDT 160 billion (approximately $1.4 billion) in charter and regasification fees since 2018, money that would not have been spent had a land-based terminal been built earlier. The IMF has flagged the energy sector’s growing financial requirements as a primary risk to Bangladesh’s debt sustainability in its consultations on the country’s $4.7 billion loan programme.

Figure 3: Annual LNG import expenditure, showing the correlation between global price movements and Bangladesh’s national import bill.

A Long Way from Qatar

The third structural condition is geographic, and it is the one the Hormuz crisis made most immediately visible.

Between 68% and 75% of Bangladesh’s LNG in recent years has come from a single country: Qatar. Add Oman, and the Middle Eastern share of total contracted supply exceeds 85%. QatarEnergy consistently delivers 40 cargoes annually under existing long-term agreements; OQ Trading delivers 16. Together, those 56 contracted cargoes represent the backbone of Bangladesh’s import programme. The reasons for this concentration are partly practical: Qatar’s North Field is the world’s largest non-associated gas field, Ras Laffan is among the most operationally reliable LNG export terminals on the planet, and QatarEnergy has been willing to sign long-term contracts on pricing terms that Bangladesh can accept. But concentration at this level means a single point of failure.

Data note: The ’68-75% from Qatar’ share needs a primary citation. Kpler trade flow data or Petrobangla’s RPGCL cargo registry are the appropriate sources. Add this before publication.

Figure 4: Supply source concentration. The right-hand panel shows how Bangladesh’s Qatar dependence compares with other major Asian LNG importers.

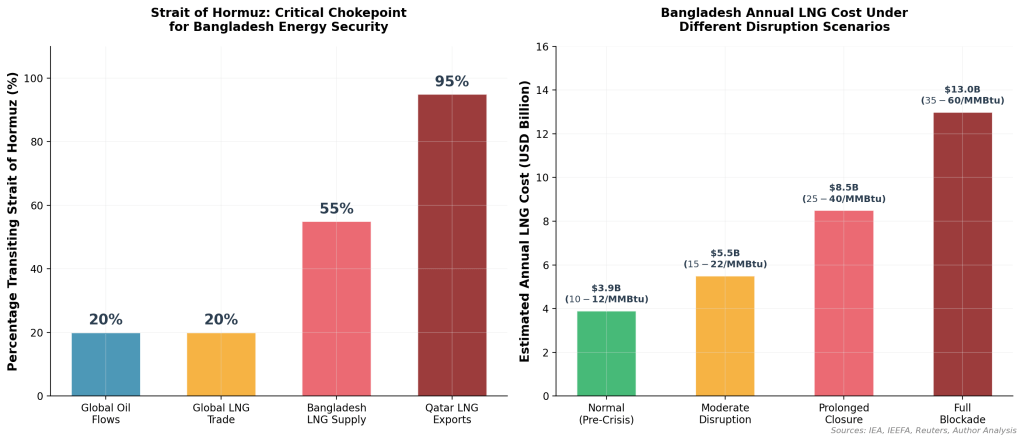

That single point of failure has a name. The Strait of Hormuz, the 33-kilometre-wide waterway separating Iran from Oman, is the only maritime exit route for Qatari, Emirati, and Kuwaiti hydrocarbon exports. Every LNG cargo bound for Bangladesh from Qatar must pass through it. Zero Carbon Analytics had noted in February 2026 that 84% of LNG shipped through the Strait is destined for Asian markets. Bangladesh, as one of the most Qatar-dependent importers in Asia, was precisely the kind of buyer that warning described.

When Iran closed the Strait on March 1, 2026, the logic of Bangladesh’s supply chain collapsed within five days. QatarEnergy invoked force majeure on March 2. OQ Trading followed on March 5. Excelerate Energy on March 6. Three suppliers, simultaneously, ceased deliveries. Of the 22 LNG cargoes scheduled for Bangladesh across March to May 2026, 18 were expected to transit the Strait of Hormuz. Almost all of them were at immediate risk.

What followed demonstrated the cost of operating without any strategic reserve. Bangladesh has no buffer storage, no underground reserves, no floating storage capacity beyond the two FSRUs already committed to regasification. With spot prices surging from $10.73 per MMBtu in late February to $28.28 per MMBtu within days of the closure, the country was forced to compete in the most expensive LNG market in recent memory, against buyers with deeper pockets, better credit ratings, and in some cases, months of reserve inventory to draw on while waiting out the crisis.

Figure 5: Chokepoint exposure and cost scenarios.

“The March 2026 crisis did not create Bangladesh’s vulnerability. It simply made it visible. The structural weaknesses had been present and compounding for years, beneath a surface of growing import volumes and signed contracts.”

Three Conditions, One Crisis

The three vulnerabilities traced in this article are not independent problems. They reinforce each other in ways that make the combined risk considerably larger than the sum of the parts.

Declining domestic production means Bangladesh must buy more LNG each year, on terms set by global markets rather than by any domestic policy choice. Having to buy more, and having to buy some of it on the open spot market, means the country is structurally exposed to price spikes it cannot control and cannot hedge against with storage it does not have. And having concentrated the bulk of its contracted supply in a single geographic corridor meant that when that corridor was closed, there was no fallback: no alternative supply contract already in place, no reserve to draw down, no domestic production to ramp up, no substitute fuel that could be brought to scale quickly.

Each of those conditions had been documented before March 2026. The IEEFA had written about the supply concentration. The IMF had flagged the fiscal risk. Energy analysts had noted the spot market overexposure. The Ramboll report had projected reserve exhaustion. None of it produced the kind of structural response that would have mattered when the Strait closed.

The question now is what a credible response looks like, and how much of the current architecture can be changed before the next disruption arrives. Bangladesh cannot drill its way out of field depletion in the short term. It cannot renegotiate contracts that are already signed. It cannot build a land-based terminal or a strategic reserve in the coming months. What it can do, and what it has not yet done at scale, is the subject of Part 3.

Coming Up in Part 3

Part 3 examines what a structurally resilient energy architecture for Bangladesh would actually require: supply diversification beyond the Gulf, the case for strategic storage, the economics of accelerating renewables as a demand-side hedge, the offshore exploration potential sitting untapped in the Bay of Bengal, and the institutional changes that would need to accompany any of it. It is not a comfortable set of options. But it is the only set available.