01 Mar

On a crisp February morning in Dhaka, the executives of ACI PLC gathered to sign a document that would have seemed improbable a decade ago. Japan’s Mitsui & Co., one of the world’s great trading houses, was extending a foreign-currency convertible loan to ACI Logistics the operator of Shwapno, Bangladesh’s largest grocery chain in what amounted to a vote of confidence in a business that had haemorrhaged money for the better part of two decades. Just four months earlier, Indonesia’s Alfamart had cut the ribbon on its first Bangladesh outlet in Dhaka, backed by a $120m joint venture involving another Japanese titan, Mitsubishi Corporation, and the Kazi Farms Group. Two Japanese conglomerates, two rival bets, one market. The question that Bangladesh’s shopkeepers (read Dokandaars), investors, and policymakers are now asking is whether either will pay off.

The answer hinges on a story that is at once familiar and peculiar the tortured, intermittently promising, and structurally fragile emergence of modern retail in one of the world’s most populous and cost-conscious nations.

The Pioneers and Their Painful Lessons

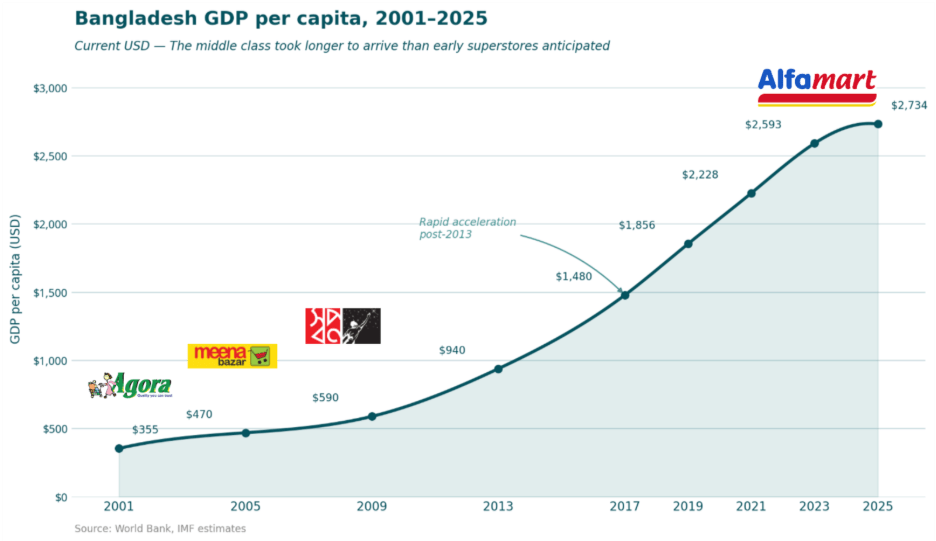

Bangladesh’s experiment with modern trade began quietly at the turn of the millennium. Agora, backed by the Rahimafrooz Group, opened its first outlet in 2001, followed by Meenabazar in 2002. These early movers were operating on the idea that a country then best known for garment exports and flood-prone flatlands would soon produce a consumer middle class eager to swap the chaos of the wet market for the cool fluorescence of a superstore. That faith was, to put it kindly, premature. But even then, modern trade was defined by this duopoly of two modern trade retail stores backed by large and well respected Bangladeshi conglomerates.

However, these two brands quickly ran into a classic roadblock. Bangladesh’s consumers are extraordinarily price sensitive. The wet market, for all its unpredictability, offers the tactile pleasure of negotiation, the comfort of credit from a familiar shopkeeper, and prices unburdened by VAT or cold chain logistics. Modern retail, by contrast, must pay for rent in increasingly expensive Dhaka real estate, sustain formal employment, maintain refrigeration, and crucially absorb a 5% VAT on packaged goods that their unorganised competitors cheerfully ignore. The tax, still unreformed, applies only to superstores and remains one of organised retail’s most perverse structural handicaps. Hence, the neighbourhood ‘Mudir Dokaan’ and the local ‘Kacha Bazaar’ always had the edge.

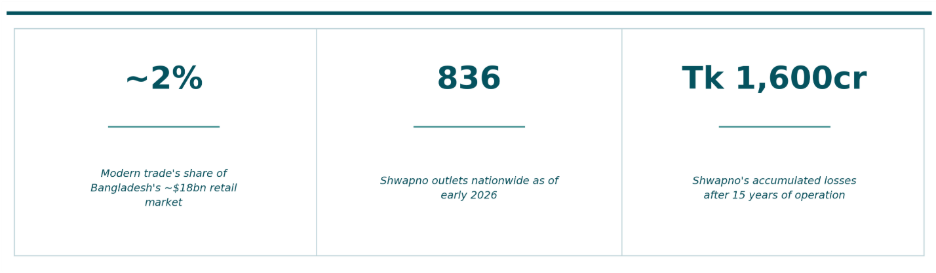

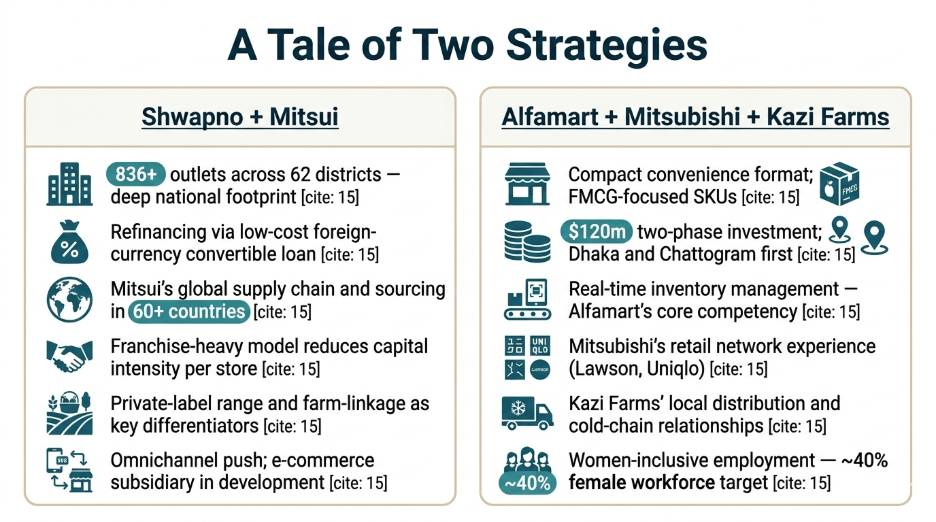

Shwapno entered in 2008 — initially branded “Fresh and Near” — as the third major chain, promising to connect farmers directly to urban consumers. It expanded aggressively. By the early 2010s the chain had dozens of outlets. It also had a near-death experience. Losses mounted. Consumer hesitation toward the superstore format, combined with logistical complexity and undercapitalisation, nearly ended the venture entirely. A leadership change in 2012 and the introduction of a franchise model from 2017 onwards eventually gave the business new life. By early 2026, Shwapno had grown to over 836 stores — by far the country’s largest chain, with more than half the modern trade market — but the debt accumulated during those expansion years had never truly been digested.

A HISTORY OF MODERN RETAIL IN BANGLADESH

| 2001–02 | Agora and Meenabazar launch; early movers bet on a middle class that has not yet arrived in sufficient numbers |

| 2008 | ACI Logistics launches “Fresh and Near,” later rebranded Shwapno; the chain expands but begins accumulating losses immediately |

| 2012 | Near-closure crisis; new leadership introduces the “loop of confidence” strategy rebuilding trust with suppliers, staff, and customers |

| 2017–18 | Shwapno launches a franchise model, accelerating store rollout without committing fresh capital to each outlet |

| 2021 | Shwapno finally records its first operating profit — though net losses persist due to crippling finance costs |

| Oct 2025 | Alfamart Trading Bangladesh Limited announced; Mitsubishi and Kazi Farms commit $120m across two phases |

| Jan 2026 | Alfamart opens its first Dhaka store, targeting urban convenience shoppers with a compact, FMCG-focused format |

| Feb 2026 | Mitsui signs convertible loan facility with ACI Logistics, injecting long-term capital and operational expertise into Shwapno |

Shwapno’s Accumulated Losses vs. Store Count

Growth without profitability defined the first fifteen years

| Year | Accumulated Loss (Tk Crore) | Store Count |

| 2011 | Tk ~200 crore | ~35 |

| 2013 | Tk ~380 crore | ~55 |

| 2015 | Tk 556 crore | ~80 |

| 2017 | Tk 759 crore | ~120 |

| 2019 | Tk ~1,050 crore | ~200 |

| 2021 | Tk ~1,350 crore | ~280 |

| 2023 | Tk 1,600+ crore | 480+ |

| 2026 | Tk 1,720+ crore (est.) | 836+ |

Source: ACI PLC annual reports, DSE filings, The Daily Star, The Business Standard

The Debt Trap and Mitsui’s Lifeline

Shwapno’s financials tell a tale that is, in its way, a microcosm of modern retail’s structural trap. The company achieved operating profitability for the first time only in 2021, more than a decade after launch. But operating profit is not net profit. Shwapno’s debt-to-equity ratio — an eye-watering 44, compared to 2.3 for Thailand’s CP ALL, which runs the 7-Eleven chain across Southeast Asia — meant that finance costs alone consumed any operational gain. By the end of FY2022-23, accumulated losses exceeded Tk 1,600 crore. The interest expense in a single year ran to Tk 154 crore. The company was, in effect, profitable in the aisle and insolvent at the treasury.

The Mitsui deal is, at its core, a refinancing story. A foreign-currency denominated convertible loan — at significantly lower rates than Bangladesh’s domestic borrowing costs — offers Shwapno relief from the compound interest spiral. The convertibility clause also holds the tantalising possibility of Mitsui eventually becoming an equity holder, aligning Japan’s largest trading house with the long-term success of the venture. Beyond the capital, Mitsui brings supply chain knowhow and sourcing muscle from operations in more than 60 countries — an asset in a market where farm-to-shelf logistics remain fragmented and wasteful.

“Of the estimated $18bn retail market in Bangladesh, modern trade’s contribution is stuck at around 2%. If the industry captures a decent 10% share by 2030, the growth potential is enormous.”

Alfamart’s Playbook: Smaller, Sharper, Indonesian

Alfamart is not a supermarket. It is, by design, something more modest and, its backers would argue, more suited to Bangladesh’s urban reality: a compact convenience store, oriented around fast-moving consumer goods, with a sophisticated IT system that tracks inventory in real time at each outlet. Alfamart operates roughly 27,000 stores in Indonesia and the Philippines, employing over 150,000 people. It is a machine built for density, margin management, and supply chain precision — qualities conspicuously absent from Bangladesh’s retail landscape.

The Mitsubishi connection is not incidental. Mitsubishi is already a shareholder in Alfamart’s parent, Sumber Alfaria Trijaya, and has extensive retail experience through brands like Lawson convenience stores across Japan and Indonesia. The $50m first phase, focused on Dhaka and Chattogram, will stress-test whether the Indonesian minimart format — predicated on compressed storefronts, limited SKUs, and relentless operational discipline — can take root in a market where the corner teashop and the neighbourhood grocery still command fierce loyalty.

Bangladesh Retail Market Structure, 2025

Estimated share of total ~$18bn retail market by channel

| Channel | Estimated Market Share |

| Traditional Wet Markets & Kirana | ~96% |

| Modern Trade (Superstores & Chains) | ~2% |

| E-commerce & Other Organised Retail | ~2% |

Source: Industry estimates, The Business Standard, TBS News

The Structural Headwinds That Neither Can Ignore

Both ventures face the same stubborn realities. The first is cost-consciousness. Bangladesh’s consumers rank among the most price-elastic in Asia. A household that earns $200 a month does not choose a superstore for the sake of air-conditioning. It chooses wherever its taka stretches furthest. The wet market and the neighbourhood grocery — unburdened by formal taxes, staff costs, or refrigeration bills — will not yield their dominance easily. The 5% VAT on packaged goods, which applies only to organised retailers, remains an active distortion that neither Mitsui nor Mitsubishi can lobby away easily.

The second is the middle class — or rather, the question of how large it actually is. Bangladesh’s GDP per capita has risen impressively, from under $500 at the turn of the century to roughly $2,730 in 2025. Headline growth, averaging over 6% annually for the past decade, has been among Asia’s most consistent. Yet the distribution of those gains has been uneven. The garment sector’s vast workforce earns wages that keep millions above absolute poverty but do not yet generate the disposable income that sustains discretionary retail. Independent economists note that the “middle class” numbers cited by retail optimists often include households whose consumption patterns remain closer to subsistence than to supermarket shopping. Bangladesh’s real middle class — households with genuine spending power for organised retail — is growing, but more slowly, and from a smaller base, than the sector’s most enthusiastic forecasters have long assumed.

Bangladesh Organised FMCG & Modern Retail Market Size

Estimated Tk Crore; growing at 10–12% annually but penetration remains exceptionally low

| Year | Estimated Market Size (Tk Crore) | YoY Growth |

| 2016 | Tk 28,000 crore | — |

| 2018 | Tk 38,000 crore | +16% |

| 2020 | Tk 49,000 crore | +13% |

| 2022 | Tk 65,000 crore | +15% |

| 2024 | Tk 78,000 crore | +10% |

| 2025 (est.) | Tk 85,000 crore | +9% |

Source: TBS News, industry estimates; modern trade penetration ~2% of total retail

There is also the question of urban real estate. Both players are targeting Dhaka and Chattogram first, cities where commercial rents have risen sharply even as the macroeconomic environment has become more volatile. Inflation in Bangladesh reached 10.87% by late 2025. The July 2024 political upheaval — which precipitated a change in government and a period of acute economic uncertainty — rattled investors and temporarily slowed consumption. The garment sector, backbone of export earnings and the primary employer of the urban working class, shed tens of thousands of jobs in the aftermath. These are not conditions in which a new retail format finds an easy footing.

Who Wins in an Aisle Fight?

The contest between Shwapno and Alfamart is unlikely to be a zero-sum affair — at least not immediately. The two chains are targeting broadly similar consumer groups by somewhat different means: Shwapno through scale and familiarity, Alfamart through operational precision and the convenience-store format that has proved devastatingly effective in Indonesia and the Philippines. The deeper competition, in the near term, is not between the two chains but between modern trade as a whole and the vast, informal, tax-advantaged ecosystem of traditional retail that still accounts for roughly 98% of the market.

The most instructive precedent may be Indonesia’s own retail evolution. Alfamart and its rival Indomaret took decades to achieve national saturation, and did so in a country with significantly higher per capita income, better infrastructure, and a more consolidated urban population than Bangladesh. The Indonesian convenience store model won by being cheaper to operate than a full supermarket and by meeting consumers where they lived — in densely packed neighbourhoods where a 200-square-foot store could serve hundreds of households. Bangladesh’s cities, choked with population and underserved by logistics, offer similar geography. The question is whether Bangladeshi incomes are yet sufficient to support the model’s economics.

Shwapno, for its part, has survived long enough to acquire something invaluable: a brand. Over 900,000 registered customers, a private-label range, and a farm-linkage network that sources more than 20% of fresh produce directly from growers give it a defensible position that a new entrant cannot replicate quickly. Mitsui’s capital injection, if it substantially reduces finance costs, could finally allow the operating profitability that the business has achieved in its aisles to flow through to its balance sheet.

“Bangladesh’s real middle class is growing — but more slowly, and from a smaller base, than the sector’s most enthusiastic forecasters have long assumed.”

Neither Japanese backer is naive about the risks. Mitsui’s investment is structured as a convertible loan — preserving an exit ramp if the bet sours. Mitsubishi’s involvement in Alfamart predates Bangladesh, and the corporation’s retail playbook is seasoned across multiple Asian markets. What is new is the convergence: two of Japan’s most powerful trading houses, effectively backing opposite corners of a market that has so far resisted the commercial logic that conquered the rest of Asia’s rising middle classes.

Bangladesh’s retail revolution has been announced, cancelled, deferred, and announced again for a quarter-century. The wet market endures. The corner grocery prevails. The superstores multiply and lose money. Now comes a fresh injection of capital, global expertise, and competitive pressure that the market has not previously seen. Whether that is enough to finally shift the balance — to coax Bangladesh’s cost-conscious consumers into the fluorescent aisles in the numbers that the models demand — will be the defining commercial question of the decade. For now, the shelves are stocked. The shoppers will decide.

This article was produced in March 2026. All financial data sourced from ACI PLC annual reports, DSE filings, and reporting by The Daily Star, The Business Standard, and TBS News. Macroeconomic data from the World Bank and IMF.