01 Mar

A Muslim-majority nation of 170 million people, blessed with fertile land and a thriving domestic food industry, exports barely $1 billion in Halal products each year. The global market is worth $2.5 trillion and growing fast. Something does not add up.

The size of the prize

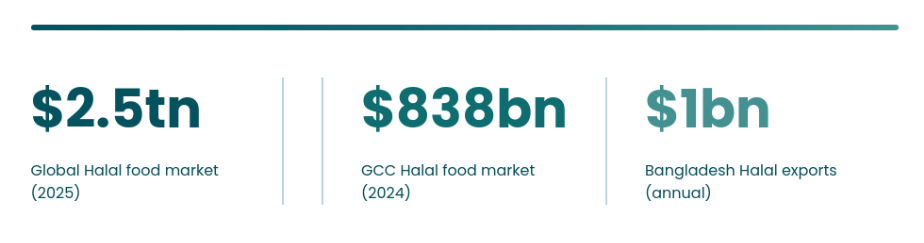

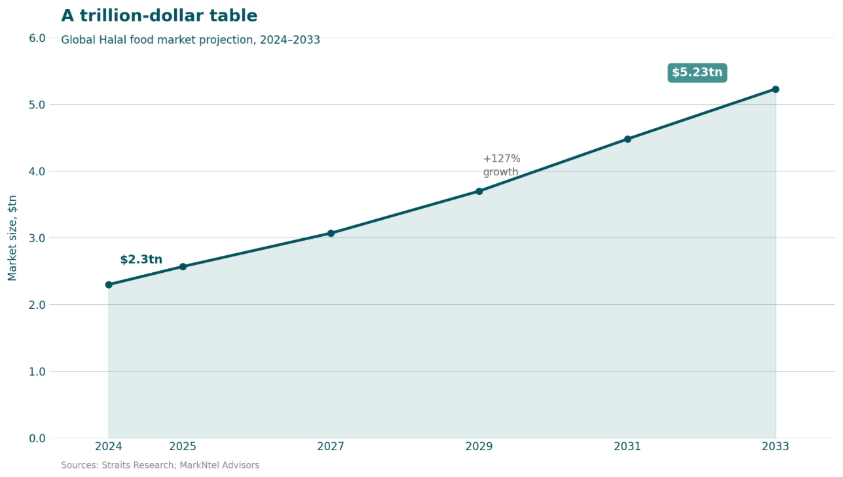

The numbers are staggering enough to make any trade minister reach for a calculator. The global Halal food market, valued at roughly $2.5 trillion in 2025, is on course to more than double by 2033, hitting $5.23 trillion according to projections from Straits Research. This is not some niche dietary preference lurking in the margins of world trade. It is a mainstream economic force, propelled by a global Muslim population that is growing faster than any other religious group, and increasingly by non-Muslim consumers drawn to Halal products for their perceived quality, safety, and ethical production standards.

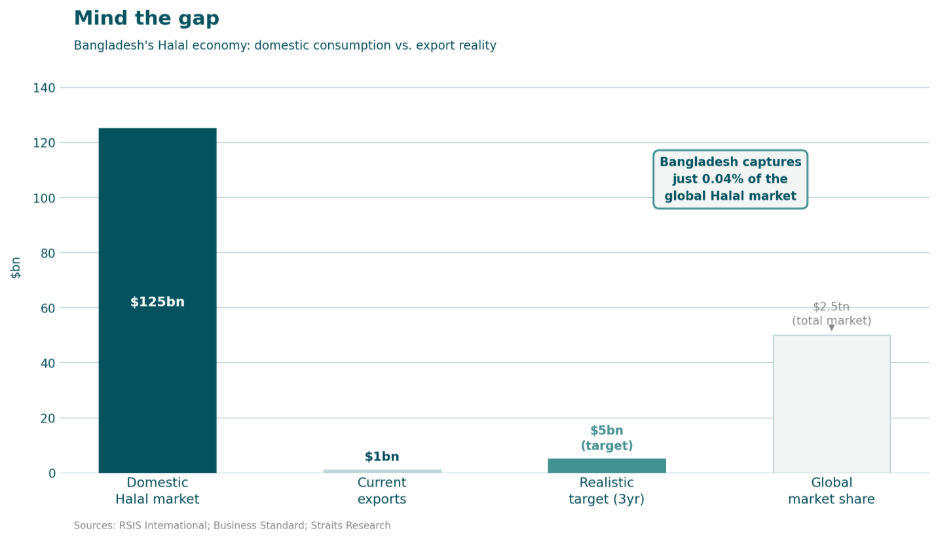

For Bangladesh, a Muslim-majority nation with a formidable agricultural base, this should be a golden opportunity. The country is already the world’s second-largest consumer of Halal products, with a domestic market valued at over $125 billion. Its farmers feed 170 million people. Its food-processing conglomerates—PRAN-RFL, Square, Akij, Olympic—are household names with decades of manufacturing experience. Yet on the global stage, Bangladesh is an afterthought. Its annual Halal exports amount to somewhere between $850 million and $1.2 billion, capturing a vanishingly small 0.04% of the global market.

To put that figure in perspective: Bangladesh exports roughly as much in Halal products each year as Malaysia earns in a single month. The disconnect between domestic capacity and international presence is one of the great puzzles of Bangladeshi trade policy—and, if the right levers are pulled, one of its most promising opportunities.

The Gulf gateway

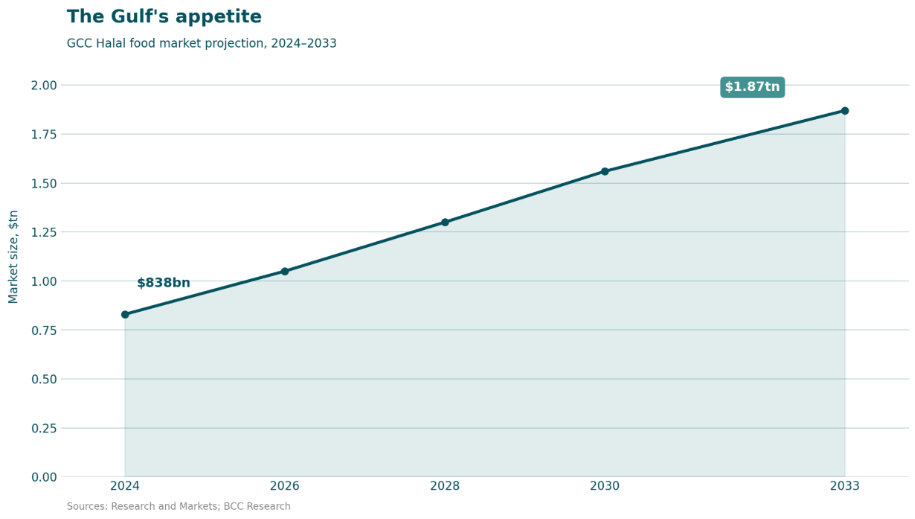

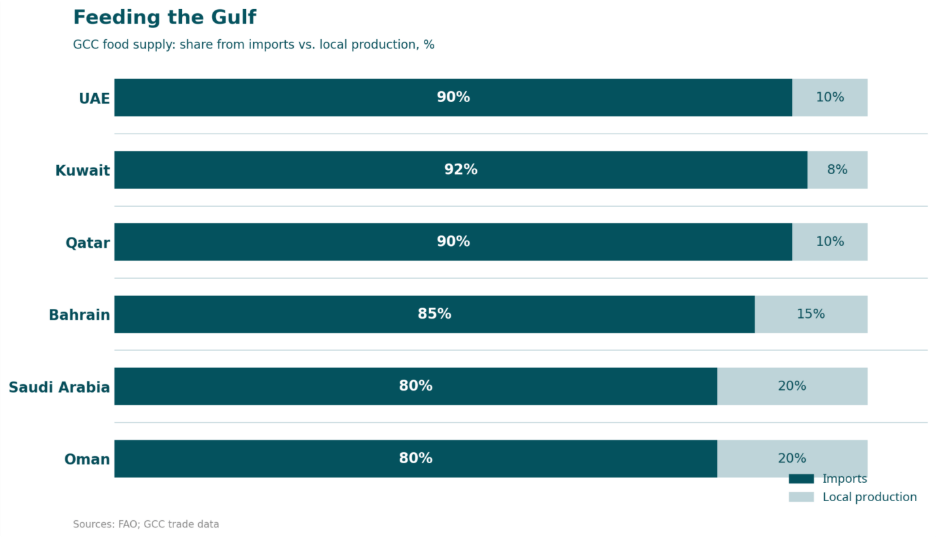

If Bangladesh is to crack the global Halal market, the Gulf Cooperation Council nations represent the most logical point of entry. The six GCC states—Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates—collectively import between 80% and 92% of their food. Their deserts may be rich in hydrocarbons, but they yield precious little in the way of agriculture. The GCC’s Halal food market alone was valued at $838 billion in 2024, and is projected to reach $1.87 trillion by 2033.

The import dependency is striking. Kuwait and Qatar import upwards of 90% of their food. Even Saudi Arabia, by far the largest GCC economy and the one with the most arable land, imports around 80%. This structural reliance on foreign food means that exporters who can meet the region’s stringent quality and certification standards have an almost captive market.

The UAE deserves special attention. Dubai, in particular, has positioned itself as the world’s pre-eminent Halal food re-export hub, a kind of Rotterdam for the Islamic economy. Products that land in Dubai do not merely serve the Emirates’ population of 10 million; they are redistributed across the Middle East, into East Africa, and increasingly to Muslim communities in Europe. Establishing a beachhead in Dubai is not just about one market—it is about plugging into a global distribution network that radiates outwards across three continents.

Bangladesh already has a foothold of sorts. The country’s large diaspora in the Gulf—numbering over 3 million workers—provides a ready-made customer base familiar with Bangladeshi brands. Ethnic grocery stores across Riyadh, Dubai, and Doha stock PRAN noodles and Akij biscuits. The question is whether this diaspora footprint can be leveraged into something much bigger: mainstream shelf space in GCC supermarkets, competing head-to-head with Turkish, Malaysian, and Brazilian imports.

Quick wins: the case for processed and dry foods

Not all food exports are created equal. Fresh produce demands cold chains, tight logistics, and razor-thin margins for error. Meat requires abattoir inspections, veterinary certificates, and a level of regulatory compliance that can take years to build. But there is a category of exports where Bangladesh could achieve rapid, meaningful gains with comparatively modest investment: processed and dry foods.

Instant noodles, biscuits, crackers, toast rusks, savoury snacks, spice mixes, and ready-to-eat meals have several decisive advantages. Their shelf life is measured in months, not days, eliminating the need for expensive cold-chain infrastructure. Their production processes are well understood by Bangladeshi manufacturers. And their unit economics improve dramatically at the scale Bangladesh’s factories can already deliver.

Consider the case of PRAN-RFL, Bangladesh’s largest agro-processor. The conglomerate already exports to over 145 countries and produces everything from fruit juices to instant noodles under a portfolio of well-known brands. Its flagship Mr. Noodles brand dominates the domestic instant noodle market. The infrastructure, the know-how, and the production capacity are all in place. What has been missing is a coherent export strategy specifically targeting GCC consumers—one that goes beyond the diaspora aisle and into the mainstream.

The formula is not complicated. Halal-certified Bangladeshi ramen, tailored to Middle Eastern flavour profiles—think saffron, sumac, and za’atar alongside more traditional South Asian spices—could carve out a distinct niche. Premium biscuits and rusks, packaged to international standards with prominent Halal certification marks recognised by GCC authorities, could sit comfortably alongside European and Turkish competitors. These are not distant aspirations. They are products that could reach market within twelve to eighteen months, given the right regulatory framework and commercial incentives.

Lost in the crowd

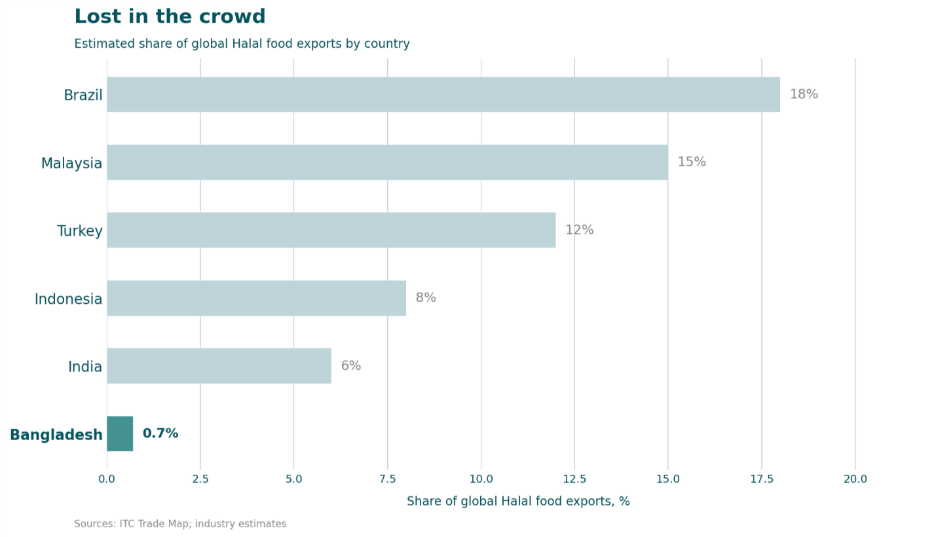

Understanding why Bangladesh has so far failed to capture a meaningful share of the Halal export market requires a clear-eyed assessment of the competitive landscape. The country is not merely competing against its South Asian neighbours. It is up against Brazil, the world’s largest Halal meat exporter and a formidable producer of processed foods; Malaysia, which has turned Halal into a national brand; Turkey, whose cultural proximity to the Gulf gives it a natural advantage; and Indonesia, a Muslim-majority giant with its own ambitions.

Malaysia’s approach is particularly instructive. Kuala Lumpur has systematically built Halal into its national economic identity, establishing JAKIM (the Department of Islamic Development) as a gold-standard certification body whose mark is recognised worldwide. Malaysia has invested in Halal industrial parks, created dedicated export-promotion agencies, and marketed itself aggressively at international food fairs. The result: a country of 33 million people captures roughly 15% of global Halal food exports, more than twenty times Bangladesh’s share.

Turkey, meanwhile, benefits from cultural and culinary proximity to the Gulf. Turkish brands are household names across the Middle East, and Istanbul’s food manufacturers have spent decades building supply chains and distribution partnerships that Bangladeshi exporters are only now beginning to contemplate.

The certification problem

If there is a single obstacle that encapsulates Bangladesh’s failure to capitalise on the Halal opportunity, it is the chaotic state of its certification regime. Two government bodies—the Islamic Foundation (IF), under the Ministry of Religious Affairs, and the Bangladesh Standards and Testing Institution (BSTI), under the Ministry of Industries—both claim authority over Halal certification. Their rivalry has produced a system that is at once duplicative and inadequate.

For exporters, the consequences are severe. Companies seeking to sell Halal products in the GCC must navigate two overlapping bureaucracies, neither of which issues certifications that are universally recognised abroad. The GCC’s own harmonised standard, GSO 2055-1, demands a level of traceability, documentation, and independent audit that neither Bangladeshi agency can consistently deliver. Exporters describe a Kafkaesque process of obtaining multiple certifications from multiple bodies, only to find their paperwork questioned or rejected at the destination port.

The contrast with competitor countries is damning. Malaysia has JAKIM. Indonesia has MUI. Turkey has its Directorate of Religious Affairs. In each case, a single, credible national authority issues Halal certifications that are recognised by importing nations. Bangladesh’s institutional fragmentation means its exporters spend more time fighting paperwork than fighting for market share.

Beyond certification, other structural barriers compound the problem. Production costs in Bangladesh remain relatively high for processed foods, partly due to the cost of imported packaging materials and flavourings. Marketing and branding capabilities are rudimentary compared to Malaysian or Turkish competitors. And the supply chain infrastructure—warehousing, quality-control laboratories, and port logistics—lags behind what is needed for reliable, large-scale food exports.

A roadmap for the Halal opportunity

Transforming Bangladesh’s Halal export potential from a talking point into a revenue stream will require coordinated action across several fronts. The good news is that none of the required interventions are technically difficult or prohibitively expensive. What they demand, above all, is political will and institutional coherence.

Unify the certification regime

This is the sine qua non. The government must resolve the IF-BSTI turf war and establish a single national Halal authority whose certification carries weight in international markets. The new body should be modelled on Malaysia’s JAKIM or Indonesia’s BPJPH—independent, technically rigorous, and staffed by professionals rather than political appointees. Its certifications must be recognised under the GCC’s GSO 2055-1 framework. Without this step, everything else is building on sand.

Target the low-hanging fruit

Bangladesh’s processed and dry food manufacturers should be the vanguard of the Halal export push. The government should provide targeted incentives—tax breaks, subsidised certification costs, and export credit guarantees—specifically for companies developing Halal-certified products for the GCC market. Product development should focus on adapting existing product lines to Gulf palates and packaging standards, not reinventing the wheel.

Invest in trade infrastructure

Modern food-safety laboratories, accredited testing facilities, and upgraded port logistics are essential. Bangladesh should also consider establishing a dedicated Halal export-processing zone, offering streamlined regulatory approvals and shared infrastructure to exporters.

Deploy economic diplomacy

Bangladesh’s embassies in GCC capitals should be equipped with dedicated trade officers focused on food exports. The government should actively engage with GCC standardisation bodies, participate in the annual Gulfood exhibition in Dubai, and pursue mutual recognition agreements for Halal certifications.

Build the brand

Finally, Bangladesh needs a national Halal brand—a recognisable mark that signals quality, authenticity, and regulatory credibility to GCC consumers. This is not merely a marketing exercise; it is a strategic investment in the country’s trade identity. “Made in Bangladesh” needs to carry the same confidence in Halal integrity that “Made in Malaysia” does today.

The sweet taste of opportunity

The global Halal food market offers Bangladesh an opportunity that is almost unique in its combination of scale, growth trajectory, and natural fit. This is a Muslim-majority country with 170 million consumers, an established food-processing industry, and a large diaspora already embedded in the Gulf’s labour markets and consumer networks. The ingredients, quite literally, are all in place.

What has been missing is strategy, coordination, and the institutional plumbing to connect Bangladeshi factories to Gulf supermarket shelves. The certification chaos must end. The export infrastructure must improve. And the country’s food manufacturers must be given the tools and incentives to think beyond the domestic market.

The Halal gold rush is real, and it is accelerating. Bangladesh can either watch from the sidelines as Brazil, Malaysia, and Turkey carve up a $5 trillion market—or it can get in the game. The first step is the simplest, and the hardest: decide to compete.

References & Sources

- https://www.prnewswire.com/news-releases/halal-food-market-on-track-to-hit-usd-5-24-trillion-by-2030—rising-muslim-population-302269837.html

- https://www.marknteladvisors.com/research-library/halal-food-market.html

- https://www.bccresearch.com/market-research/food-and-beverage/halal-food-mena.html

- https://www.researchnester.com/reports/halal-food-market/6061

- https://www.businesswire.com/news/home/20251113295458/en/Global-Halal-Economy-Industry-Research-Report-2025-A-$10.5-Trillion-Mar

- https://www.researchandmarkets.com/report/middle-east-halal-food

- https://rsis.edu.sg/rsis-publication/rsis/rsis-international-halal-food-products-adoption-bangladesh-2025/

- https://www.tbsnews.net/economy/trade/bangladesh-exports-halal-products-worth-around-usd-850-million-annually-1123456

- https://www.tbsnews.net/economy/halal-products-export-receives-boost-new-policy-more-required-987654

- https://straitsresearch.com/report/halal-food-market

- https://www.gminsights.com/industry-analysis/halal-foods-market

- https://muslimnetwork.net/2026/bangladesh-halal-exports-stalled-rival-certification

- https://halalfocus.net/2026/halal-certification-dispute-if-bsti-exporters-limbo/

- https://vietnamnews.vn/economy/1698452/bangladesh-missing-out-3-trillion-global-halal-market.html