22 Feb

Over the last decade, thematic bonds including green, social, sustainability, and sustainability linked instruments have moved from a niche market to a major part of sustainable finance and capital markets. (OECD) For Bangladesh, where sustainable finance demand is rising across WASH, climate resilience, renewable energy, and CMSME portfolios, issuing a USD denominated thematic bond represents both an opportunity and a structural challenge. A key strategic question now confronting Bangladeshi issuers is whether they should onboard a multilateral or development finance backed credit guarantor when accessing international USD markets. (OECD)

Drawing on insights from a recent Singapore capital markets mission and a review of global literature and emerging market precedents, this article presents a balanced assessment of the pros and cons of using partial credit guarantees in USD thematic bond issuance.

The Context Why USD Thematic Bonds Are Structurally Different

Bangladeshi banks and corporates operate in a domestic environment where issuer ratings are often constrained by country and sovereign ceiling dynamics, which can limit how global investors view standalone risk. (UNDP)

USD liquidity is externally influenced, and investor familiarity with Bangladesh risk remains limited relative to larger and more frequently traded emerging markets. At the same time, hedging tools exist but hedging can be difficult to execute at scale in many emerging market settings, particularly when cost, market depth, and operational constraints are considered. (IMF eLibrary)

When issuing in local currency, domestic institutional investors often absorb supply. However, a USD thematic bond listed in markets such as Singapore or Luxembourg enters a global risk benchmarking ecosystem where investors compare it against similarly rated issuers across regions.

During discussions in Singapore with arrangers, ESG investors, and exchange officials, one consistent theme emerged: thematic labelling alone does not reduce credit risk perception. Investors still expect credible use of proceeds rules, external review practices, and transparent reporting, as reflected in widely used market principles and guidance for thematic bonds. (ICMA) Pricing, however, ultimately depends on credit strength, and investors price macro and country risk separately from the label. (OECD)

This is where credit enhancement enters the discussion.

The Case For Onboarding a Credit Guarantor

1 Improved Credit Strength and Potential Pricing Efficiency

A partial credit guarantee is a well established credit enhancement mechanism for debt instruments including bonds, typically covering a defined portion of debt service or principal and or interest. (World Bank) In practice, an appropriately structured guarantee can improve how the bond is perceived by investors, and may expand the set of portfolios that can consider the instrument, especially where mandates impose minimum credit quality thresholds.

Several investors in Singapore noted that mandates often include minimum rating or internal credit policy thresholds. A guarantee can therefore expand the eligible investor base, particularly among more conservative institutions.

2 Investor Base Diversification

Without enhancement, many global funds categorize exposure to smaller or less frequent issuers as frontier risk. A credible guarantee can shift the risk calculus by changing the perceived probability of loss on the guaranteed portion and strengthening confidence in repayment mechanics. (OECD)

This can be relevant for debut USD issuances, where building investor trust is a practical hurdle beyond thematic labelling alone.

3 Anchor Effect and Signaling Value

When a credible multilateral or development finance linked guarantor participates, it can signal additional due diligence and structured risk analysis. This is often cited as a catalytic feature of guarantees in blended finance and sustainable finance transactions. (OECD)

In emerging markets, early thematic issuances have sometimes used guarantees as a market building bridge, especially for demonstration transactions intended to catalyze follow on activity. (cdkn.org)

4 Mitigation of Refinancing Risk

For banks deploying proceeds into longer tenor WASH, climate, or infrastructure assets, a partial guarantee can support longer tenor funding structures and reduce rollover stress, particularly when market liquidity tightens. This aligns with the general rationale for partial credit guarantees as mechanisms to improve market access and borrowing terms. (World Bank)

The Case Against Credit Enhancement

While the benefits are compelling, there are equally important counterarguments.

1 Cost of Guarantee Fees and Total Transaction Costs

Guarantees involve fees and transaction costs, and guarantee providers explicitly price the risk they take. (IFAD) In addition to guarantee fees, issuers must often account for legal, documentation, and structuring costs associated with multi party arrangements across jurisdictions.

When combined with arranger fees, listing costs, external review costs, and ongoing reporting, total issuance costs can become substantial. If the pricing benefit and investor access benefit do not sufficiently offset these costs, the net economic value may be marginal.

During Singapore discussions, some arrangers cautioned that for well managed banks with comparatively strong balance sheets, the incremental spread benefit may not always justify the additional cost and complexity.

2 Structural Complexity and Timeline Risk

Introducing a guarantor typically adds structuring layers. Partial credit guarantees are not simply an add on, they often require additional due diligence, legal negotiations, and alignment on covenants, eligible assets, and reporting requirements. (World Bank) For issuers trying to hit a specific market window, this can extend timelines and increase execution risk.

3 Dependency Risk and Market Signaling

There is also a strategic concern: repeated reliance on enhancement may lead investors to anchor expectations around guaranteed structures, which can complicate a longer term transition to standalone issuance. Many countries and issuers pursue a sequencing approach where early transactions are more supported and later transactions rely more on standalone credit once familiarity improves. The broader point that guarantees can play a catalytic but transitional role is well documented in market building and blended finance literature. (cdkn.org)

4 Moral Hazard and Asset Discipline

Guarantees can change the distribution of risk, which can reduce the intensity of investor scrutiny on the underlying pool if the structure is not designed carefully. This is why market guidance emphasizes that credibility and transparency mechanisms including external reviews and post issuance reporting remain essential regardless of enhancement. (ICMA) A guarantee should complement robust underwriting rather than substitute for it.

Strategic Considerations Specific to Bangladesh

Given Bangladesh’s macroeconomic environment and the realities of sovereign ratings and ceilings, USD issuance carries an additional layer of country risk perception that investors typically price independently. (Fitch Ratings)

Key strategic questions include:

- Is this a debut issuance in USD markets?

- Is the issuer seeking to access conservative global funds with strict mandate constraints?

- Are the proceeds allocated to climate or WASH portfolios with measurable impact?

- Does the expected pricing and distribution benefit meaningfully outweigh guarantee and execution costs?

- Is there a longer term plan to graduate toward standalone issuance?

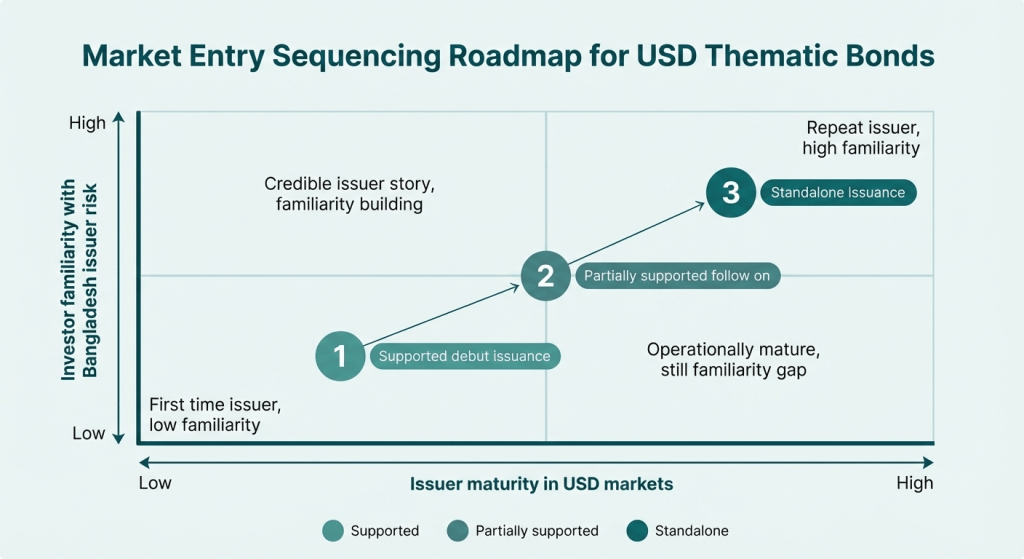

Figure 1: Market Entry Sequencing Roadmap for USD Thematic Bonds

For first time USD thematic bonds, particularly where global ESG appetite is present but risk tolerance is calibrated, a partial credit guarantee can function as a bridge instrument.

However, for repeat issuers with demonstrated reporting discipline, transparent impact metrics, and strong balance sheets, a standalone approach may be strategically preferable.

Lessons From Singapore and Global Literature

Three consistent themes emerged from engagement with Singapore based investors and from widely used market guidance:

Thematic credibility is increasingly treated as a baseline expectation, and external reviews plus transparent reporting are central to that credibility. (ICMA)

Investors price macro and credit risk separately from the ESG label, so the label does not erase country risk. (OECD)

Guarantees often work best when placed inside a broader strategy that uses transitional structures to build market access, rather than as one off risk transfer mechanisms. (OECD)

A Balanced Conclusion

Do Bangladeshi issuers need a credit guarantor for USD denominated thematic bonds

The answer is conditional, not universal.

Credit enhancement makes strategic sense when the issuance is a debut transaction, when investor mandates require a meaningful uplift in perceived credit strength, when the distribution benefit is large enough to justify the added cost and complexity, and when the objective is market entry and credibility building. (World Bank)

Credit enhancement may be unnecessary when the issuer already has investor familiarity, when the cost benefit outcome is marginal, when the objective is long term standalone market positioning, or when structuring complexity outweighs the advantages. (OECD)

For Bangladesh’s evolving sustainable finance ecosystem, the decision is strongest when framed as part of a multi issuance roadmap rather than a single transaction lens.

Ultimately, the question is not whether guarantees are good or bad, but whether they are strategically optimal at a given stage of market development. As Bangladesh integrates more deeply into global ESG capital markets, credit enhancement can serve as a catalytic bridge, helpful in early stages, but not a permanent substitute for institutional credit strength, disciplined asset governance, and consistent post issuance reporting. (cdkn.org)

Reference list

- International Capital Market Association, Green Bond Principles and guidance on reporting and transparency. (ICMA)

- ICMA, External Reviews guidance for thematic bonds. (ICMA)

- OECD, Trends in the sustainable bond markets (2024 shares and market context). (OECD)

- World Bank Group, Partial Credit Guarantees description and mechanics. (World Bank)

- MIGA, Partial Credit Guarantee for Bonds product overview. (miga.org)

- Asian Development Bank, Partial Credit Guarantee brochure. (Asian Development Bank)

- OECD, The role of guarantees in blended finance. (OECD)

- CDKN, Enhancing green bond issuances in developing economies (market building and catalytic role). (cdkn.org)

- OECD, Green social and sustainability bonds in developing countries (example of credit guarantee role in a Kenya case). (OECD)

- UNDP, Development context of sovereign credit ratings and rating ceiling concept. (UNDP)

- Fitch Ratings, Bangladesh sovereign rating action (context on sovereign rating level). (Fitch Ratings)

- Moody’s rating ceilings and Bangladesh ceiling discussion (local currency and foreign currency ceilings). (Moody’s Ratings)

- IMF, Managing foreign exchange rate risk (overview of hedging considerations in public debt contexts). (IMF eLibrary)

- African Development Bank, policy document indicating guarantee fee pricing approach. (afdb.org)